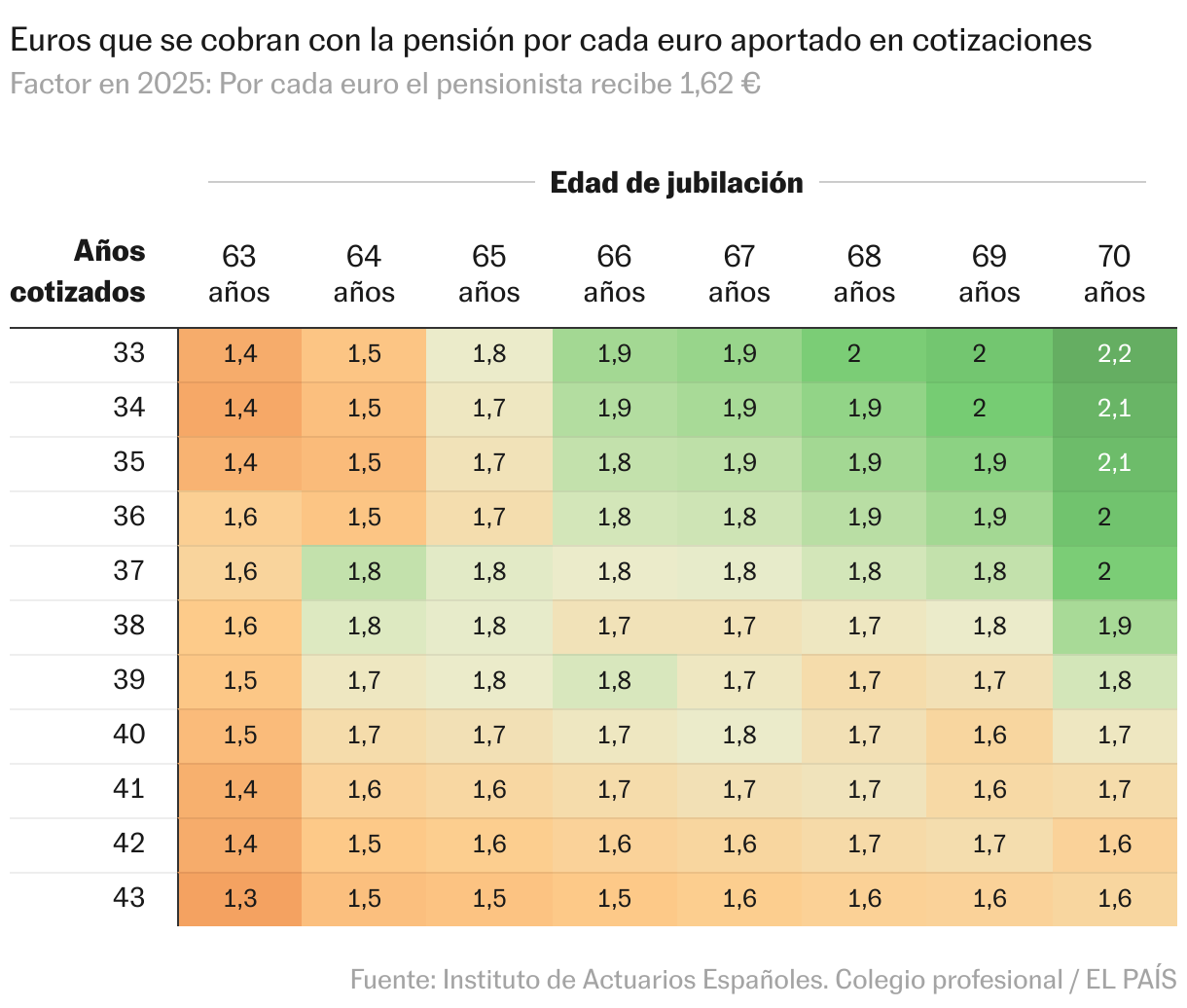

Most workers have the perception that, once retired, it receives money similar to that they have contributed with their quotes throughout their working life. However, in general that is not so. A type worker who has had an uninterrupted work career between 33 and 43 years quoted, and who retires today with between 63 and 70 years, will receive with the collection of his pension in what remains of life of life an average of 62% more than he has contributed to the system in social quotes when he was active.

This is determined by the latest report of the Actual Research Center of Spain, to which this newspaper has had access, and that analyzes the relationship between what is contributed in contributions and what a worker will receive that retires in 2025 and compares it to what that relationship was like five years ago. Specifically, the actuaries – which are the professionals who analyze the risks and uncertainty of future situations, using mathematics, statistics and financial theory – have measured, as they have done in other years, this degree of generosity through what they call Actuarial equity factorwhich determines how many euros a type pensioner is taken for each euro contributed to social security. That said, they warn that this indicator measures only that of the types of types that retire in a given year and taking into account only the retirement pension.

The result of the comparison with respect to 2020 is that the generosity of pensions has grown, since five years ago, for each euro contributed, this type worker who retired would then receive 1.55 euros (or what is the same a 55% more than admitted to the Social Security Fund). In this way, the report draws attention to the fact that pensions are more generous with the individual individuals in spite of the latest pension reform (of 2021 and 2023) aimed at guaranteeing the sustainability of pensions with measures to increase income, harden access to early retire purchasing power Some of these adjustment measures, in actuarial terms, make the relationship between the euros provided and those that will be received more demanding.

In fact, the director of the Activatory Social Welfare Observatory of this Research Center, Gregorio Gil de Rozas, points out that the latest reforms “were well oriented in actuarial terms.” These terms pursue that “the system returns in the form of a pension exactly the quoted, without generating deficit or surplus, which would be facing an actuarially fair system,” says this academic work. And it is that if in the analysis of the relationship between the paid and what was received, only the update of the pensions with the CPI and the rest of the measures of the most recent reforms cited, the result would be that for each euro contributed the pensioner would receive 1.52 euros, a little less than the 1.55 euros of 2020. If in addition to the revaluation with inflation and the effects of the latest reforms, the effect of aging is incorporated, this indicator goes to 1.55. But it is also applying the lower GDP growth forecasts, when the relationship between what is contributed and what will be received makes the leap to 1.62.

So what happened so that the pensions of a type worker are more generous now than five years ago, despite the adjustments made by the reforms? The analysis points to the impact of two exogenous factors to the pension system: on the one hand the aging of the population (life expectancy from 65 years according to the tables used in 2020 was 21.14 years compared to 21.52 years according to those used in 2025); and, on the other hand, the lower projection of the planned GDP (the new forecast of real growth in the future according to the Ageing Report of 2024 that the European Commission elaborates, it is significantly lower than the forecast that was used in 2020 based on the Ageing Report of 2018).

According to all this, the authors of the document conclude that “the pension reforms of 2021 and 2023 have been insufficient and have failed to stop the tendency towards greater imbalance” of the system. Although they admit that “with respect to 2020, the reforms have reduced generosity in some cases, especially in workers with short labor careers or early retirements (and have closer more pensions to balance). However, they have not been enough to counteract the impact of aging and the least expected economic growth. ”

Gil de Rozas also highlights that this report also shows that some aspects of the latest pension reforms have slightly improve the equity in the type retirees that were withdrawn 2020 and in those who are going to do it in 2025. This means that the treatment of the different contribution races that retire in the same year is now more homogeneous than five years ago. And this is due to the increase in ordinary retirement age since short labor careers have worsened their treatment by assigning them the percentage of quoted years, “the study indicates.

Likewise, the actuaries have made a projection of what will be the relationship between what was contributed and what was received by 2045 and 2065, resulting in an even more generous and, therefore, with greater actuarial imbalance. Specifically, the actuarial equity factor will go from 1.62 from 2025 to 2.14 in 2045 already 2.20 in the year 2065 (without taking into account the closing clause that could be forced, as of this year, to take income measures, cost of expense or both things). In this sense, these professionals point out that “the reforms of the system planned for the future can barely do anything against this trend, to which the progressive increase in life expectancy is added.”

Finally, the conclusion that this group of researchers draws is that “for a new reform of the pension system to be effective in terms of financial sustainability and equity in the distribution of efforts, it should contain automatic adjustment mechanisms before changes in long -term economic growth and in life expectancy”, as they have done in other countries of the European environment, they add. In the absence of these automatic adjustments – the current closure clause of the intergenerational equity mechanism is only semi -automatic – “the pension system will continue to need increasing transfers of the State to maintain a level of growing generosity over the years.”