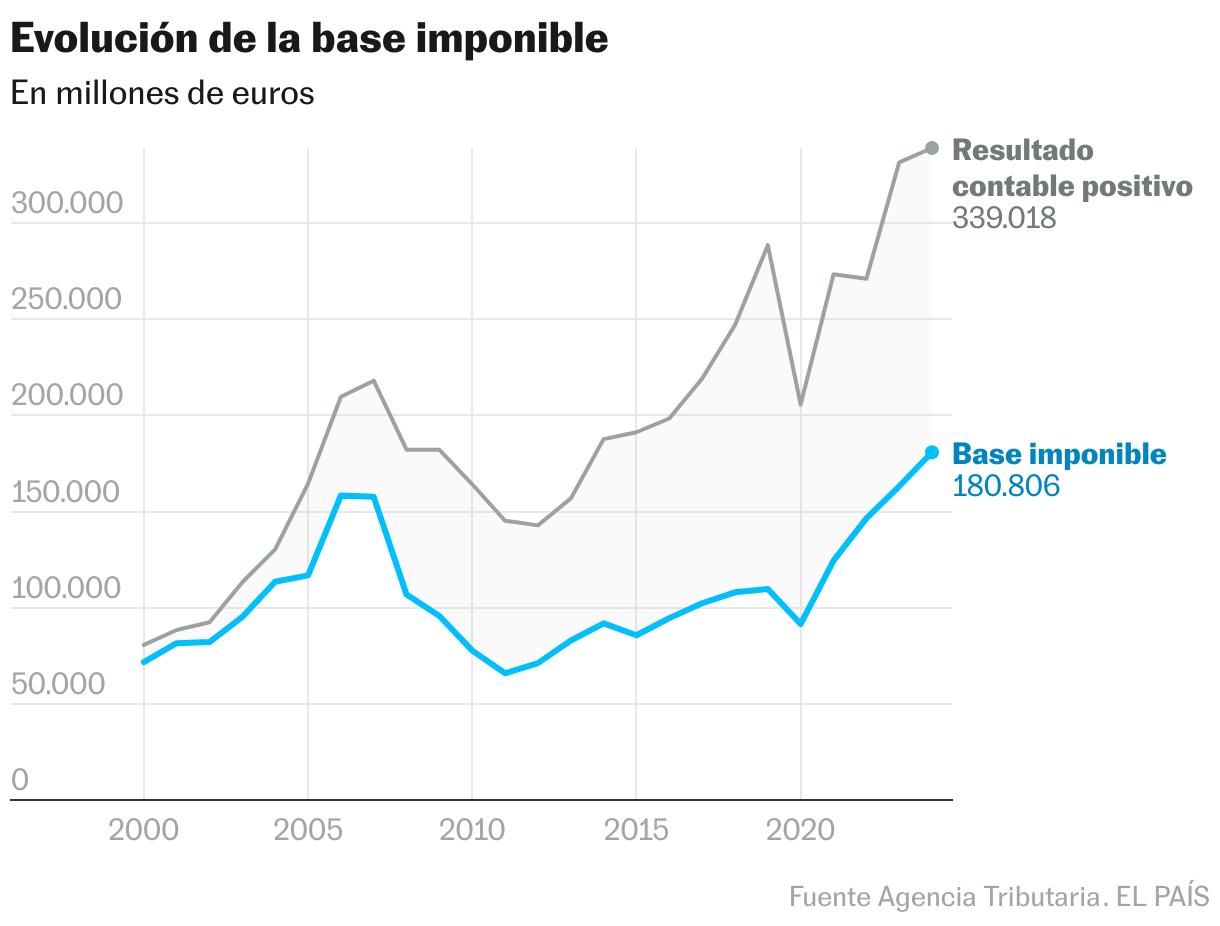

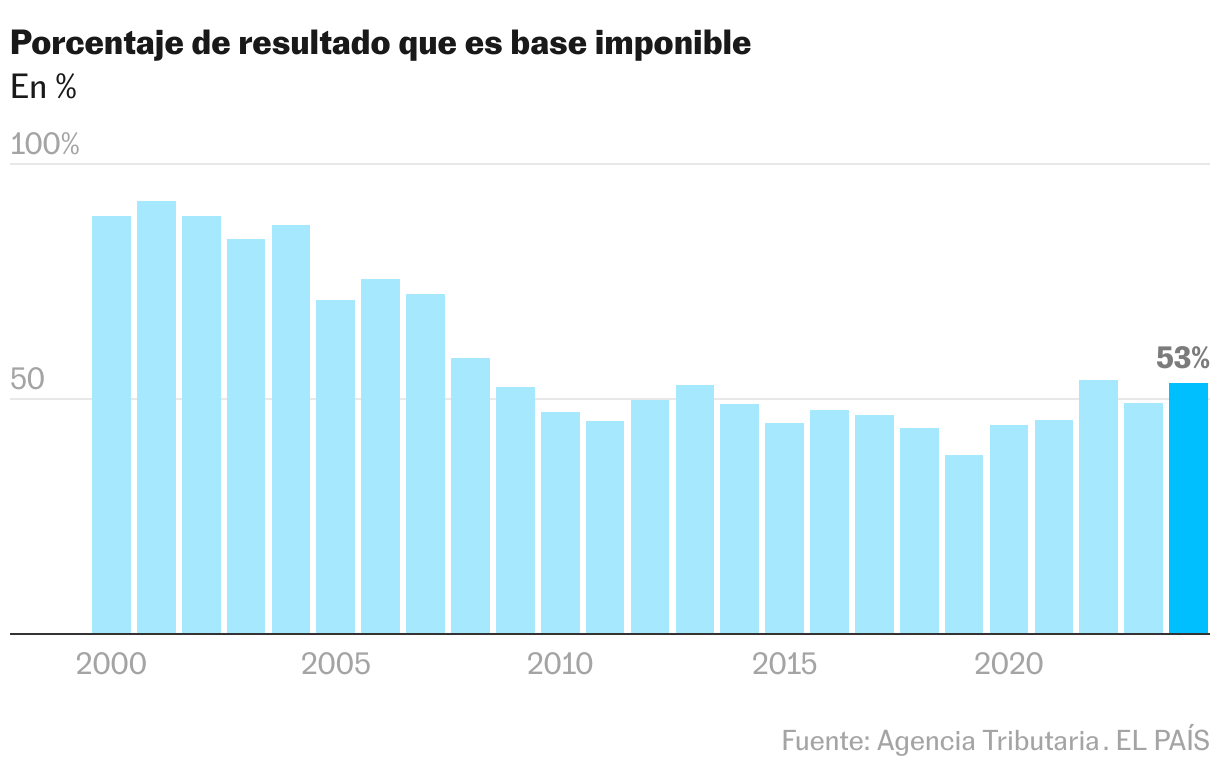

If a company obtained a net profit of 100 euros, only 53 would be; The rest would be outside the fiscal calculation. Companies in Spain manage to significantly reduce the part of their profits on which it is applied, which enlarges the gap between its accounting results and its taxable bases and limits the public collection of one of the great tax figures of the country. And they achieve it through perfectly legal mechanisms, designed to encourage some aspects of economic activity or to cushion the losses of the crisis years. In 2024, companies reached net income of 339,018 million euros, the highest figure in history. However, only 180,806 million (53.3%) were subject to taxation, which means that almost half of the benefits managed to dodge the tax tax, according to data published this week by the Tax Agency. The greatest mino occurred for the benefits from the outside of the subsidiaries of the large Spanish companies, which are already taxed in the countries where they are established.

This lag, which has been installed in the Spanish tax system for more than 15 years, is a consequence of a network of fiscal mechanisms to reduce its tax burden, mainly through the compensation of negative tax bases, which operate as past losses, and exemptions on international income.

The historical evolution of this gap is clear. Between 1995 and 2008, the benefits and quantity on which the tax is calculated advanced almost parallel, with about 80% of business income subjected to taxation. In fact, for several years 90%was exceeded. However, the financial crisis and the subsequent outbreak of the real estate bubble marked a turning point: the proportion clearly fell below 50%. The economic difficulties that Spain crossed pushed the internationalization of a part of the productive sector in search of business and the influx of benefits from abroad began to shoot since then. From there there was a slight approach between the result and the base, although experts believe it is difficult to return to the levels prior to the crisis. The high burden of accumulated tax credits and the internationalization of companies prevents its maximum collection potential from reaching.

To understand why the gap between both concepts – the accounting and tax base result – does not stop widening, you have to go back to the 2008 crisis and the generation of a huge tax credit bag. These accumulated losses remain a ballast for collection, by allowing companies to reduce, although now with greater limits, their tax bill charged to past exercises.

The mechanism by which these discounts operate is simple. As Francisco de la Torre, Anspector de Finance and author of And this, who pays it? (Debate), companies registered billions in losses during the crisis and scored them in their balance sheets. Today, these negative tax bases remain in force and can be compensated year after year, which allows to reduce the amount over which taxes are effectively paid by subjecting an increasing percentage of the benefits declared by companies. ” Another mechanism, remembers the tower, are the dividends and surplus value obtained abroad, which are exempt. When these concepts are combined, the inspector continues, the erosion of the taxable bases “is simply brutal.”

For Violeta Ruiz Almendral, professor of Tax Law at the Carlos III University of Madrid, it is not entirely appropriate to compare the positive accounting result of companies with their taxable bases, since these are built on the profit and loss account and carry out a series of adjustments. Some, such as the exemption of the income generated abroad, are “a commitment to the internationalization of the companies that have been very good for Spain.” Others, such as the compensation of negative tax bases, have to do with an adequate taxation of the income, since if a company cannot compensate losses, it would be paying for an “that is not real” income. Therefore, he defends, “the real benefit of a society is not necessarily the accounting result, nor is the tax base necessarily.” By design, “the accounting result and the tax base will be different.”

In addition to these formulas, companies also have the consolidation adjustments, which apply fiscal groups with the aim of avoiding the double imposition of the benefits declared by the companies of the same group. And they enjoy, in turn, a broad set of fiscal or extra -constable adjustments, whose main objective is to consider the differences of treatment between accounting and prosecutor so that the taxed corporate income approaches more appropriately to the taxpayer’s economic capacity. Therefore, he insists of the tower, aspiring to the collection of the years prior to 2008 “is not realistic.”

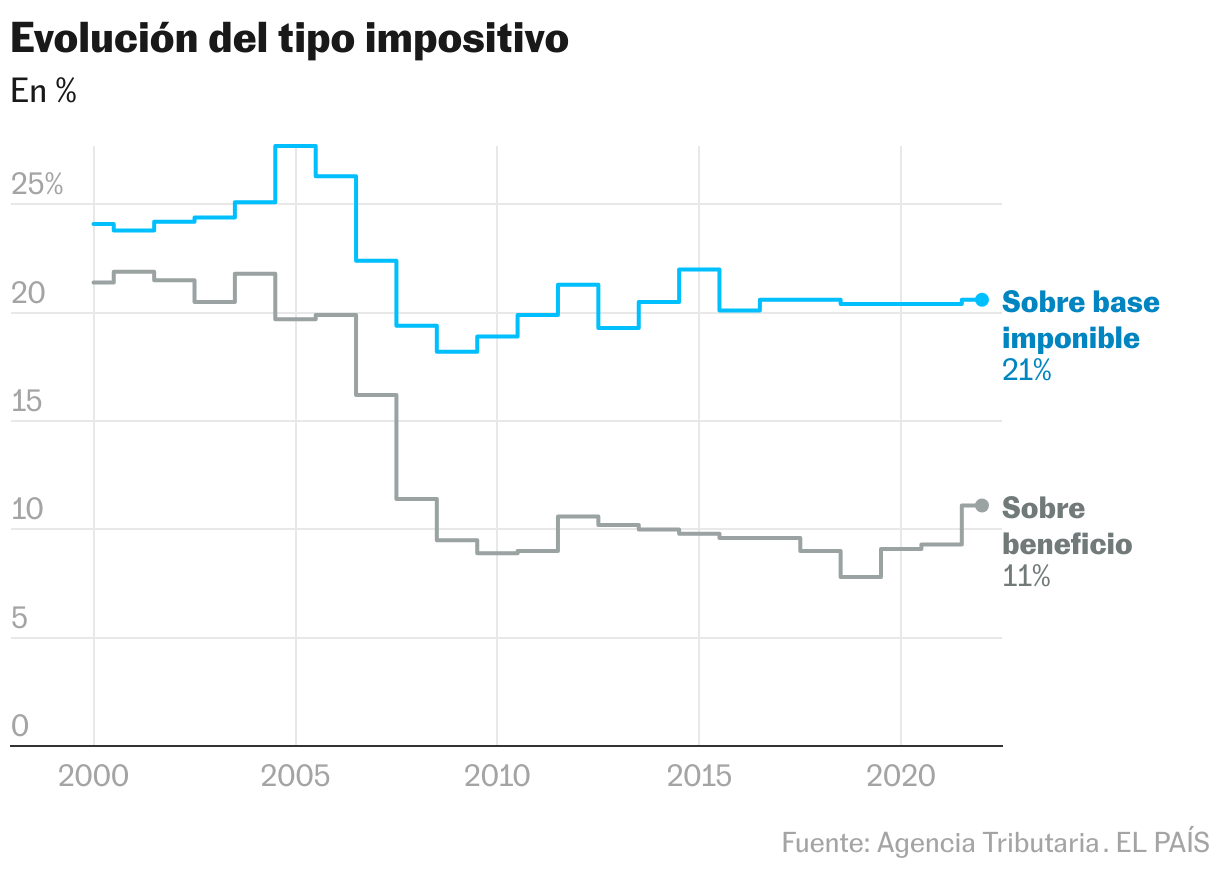

The mechanisms of which companies are nourished make them, which is the percentage of taxes that are really paid, differ greatly depending on whether the benefit or tax base is taken into account. In the second case, the average type was in 2024 of 20.2%, but fell strongly to 10.8% if the positive accounting result is taken into account.

All this led to the Corporation Tax, the highest figure for almost two decades, but still away from the almost 45,000 million that were recorded in 2007. And all this in a context marked, among other aspects, due to the limitation in the compensation of negative tax bases that affected large groups, so that revenues, in normal conditions, would have been lower.