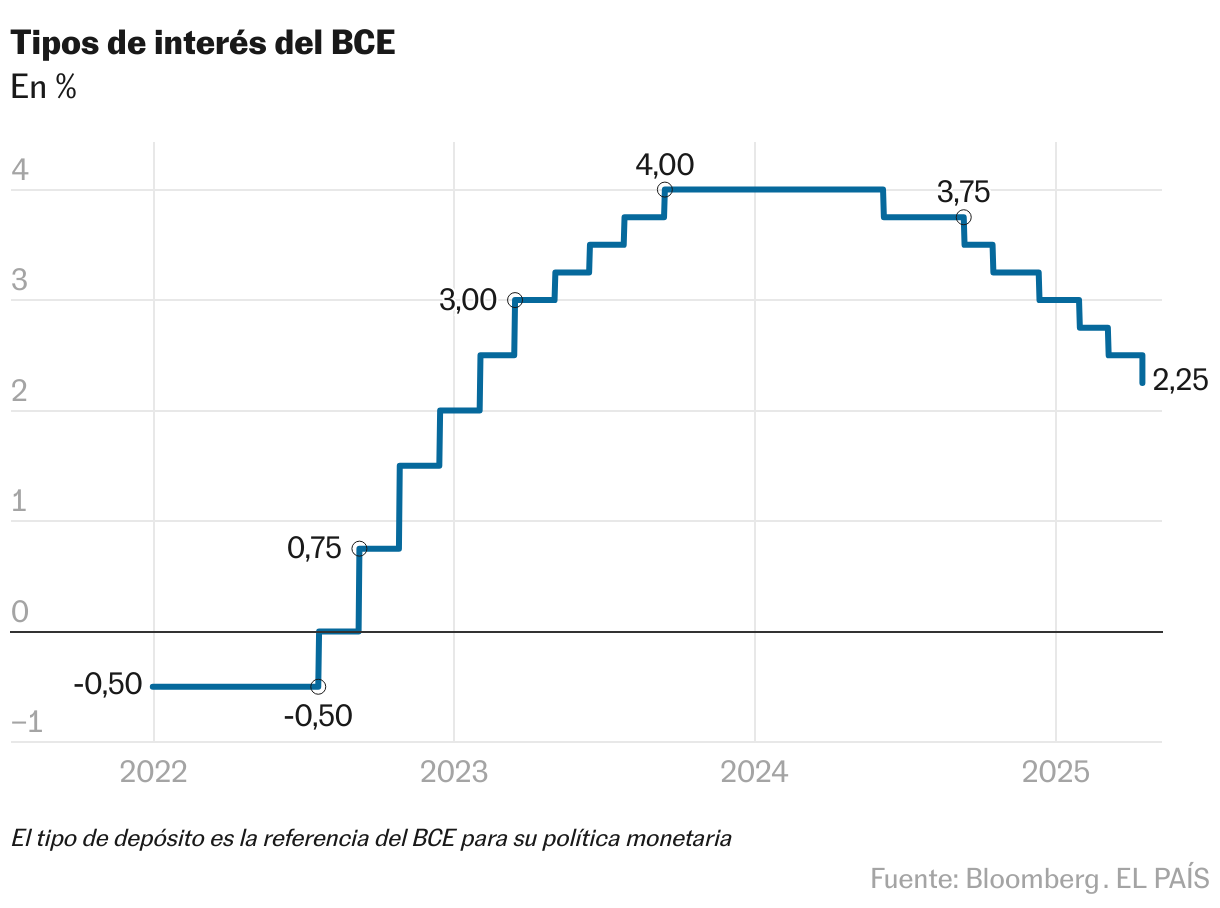

Donald Trump inclines the balance. The European Central Bank has trimmed interest rates at 25 basic points for the sixth consecutive time, up to 2.25%, in a movement propelled by the US president. The last time Christine Lagarde went through a press conference, six weeks ago, the possibility of making a pause seemed feasible. Until probable, given the change of language, the ambitious spending plans in Germany, and the highest speed of monetary softening undertaken by Frankfurt compared to other large central banks, much more reluctant to lower the price of money. But on the return of the French to an appearance, the world seems another.

In its statement, the Eurobanco highlights the advances in the fight against inflation – which fell a tenth in March and closed by 2.2%, very close to the objective – but recognizes that “the growth prospects have deteriorated due to the increase in commercial tensions”. That greatest uncertainty, and the adverse and volatile response of the threat markets, follows the text, with causing a hardening of financing conditions, and all these united factors “could additionally ballast the economic perspectives of the euro zone,” he warns in his message, from which the references to that the types are at “considerably less restrictive” levels have disappeared.

Something has broken in the machine room of capitalism. It is not irreparable, given the self -inflicted character of the damage – Trump will not be eternal – and its permanent capacity for reinvention against the crises -, ironized at the beginning of the great recession an Italian politician, Gianni Ruffulo – but can leave scars beyond his mandate, especially in the US if suppliers and investors go with music elsewhere. The White House has launched an asymmetric, high -impact trade war for China and less intensity – now – towards the rest. The economic order based on political multilateralism and economic globalization trembles and turns towards a dynamic of blocks that are replicated, shortening and diversifying their supply chains, and ultimately reduce external units. That means the end of a whole series of efficiencies: less cheap Russian gas and less US military umbrella for Europe, fewer Asian products at low cost for the US.

While the old does not just die and the new does not end up, the negative effects of that change of paradigm for growth, in the twenties, the fall of energy prices and the rise of the euro against a dollar in low hours, have ended up convincing the Governing Council of the ECB that the great threat that is now looming on the European economy is not a new rebound of prices, but the stagnation, but the stagnation, but the stagnation removing ballast so that financing flows to companies and homes, encouraging consumption.

With the financial markets plunged in a roller coaster – with more pending descendant than increases – by the succession of tariff and truce ads from the oval dispatch, the indicators of trust and growth collecting in Germany, the first continental economy ——, and international organizations, from the WTO, to the IMF, passing through the UN, warning of the deterioration of the deterioration of the global economy, the ECB Margin for inaction. In fact, the criticisms prior to the meeting went more on the opposite side, accusing the Eurobanco of passing from cautious and dropping if it would not be more effective to lower two steps in one jump and cut the types in 50 basic points of a pull, given the exceptionality of the moment.

The currency market presses in that direction. The euro is 10% up against the dollar since the beginning of the year. That means cheaper imports to Europe, and therefore less inflation. Gas quotes (-40% from February peak) and oil (-13% this year) also contribute. And the Euribor, the lower the more the types fall, when deducing a more lax monetary policy.

The ECB, however, could also have resorted to a more conservative argument to justify a pause. This was done this week by the Bank of Canada, which surprised to maintain the intact types after seven cuts and shielded that the uncertainty about tariffs makes it impossible occur. And so it seems that the US Federal Reserve will do it: in a speech this Wednesday, its president, Jerome Powell, was in favor of waiting for more “clarity” in the current economic policy to move the price of money. Trump reacted this Thursday asking for his dismissal for not acting.

It has been a relief for markets, but the end of history is yet to be written. And for the moment the ECB cannot include in its mathematical models long -term tariff figures. That weakens its capacity for analysis and anticipation of trends, but a priori its position is somewhat more comfortable than that of the Fed, on which a stagflation scenario plans. The nightmare of any central banker.

[Noticia de última hora. Habrá actualización en breve]