Housing for rent has been consolidated as one of the preferential destinations for a scenario marked by financial uncertainty. Within the residential sector, the lease market has gained weight as a refuge value for both large funds and companies and small homemade, due to a context of sustained demand, limited supply and. Rentist logics after the rise of this business have intensified interest in understanding not only how much they earn by renting, but also where. In that question – apparently simple. The last data remittance published by the Tax Agency shows a divergent behavior between the center and the periphery of the big cities, where the profitability obtained by the owners does not always correspond to the visibility or apparent prestige of each neighborhood.

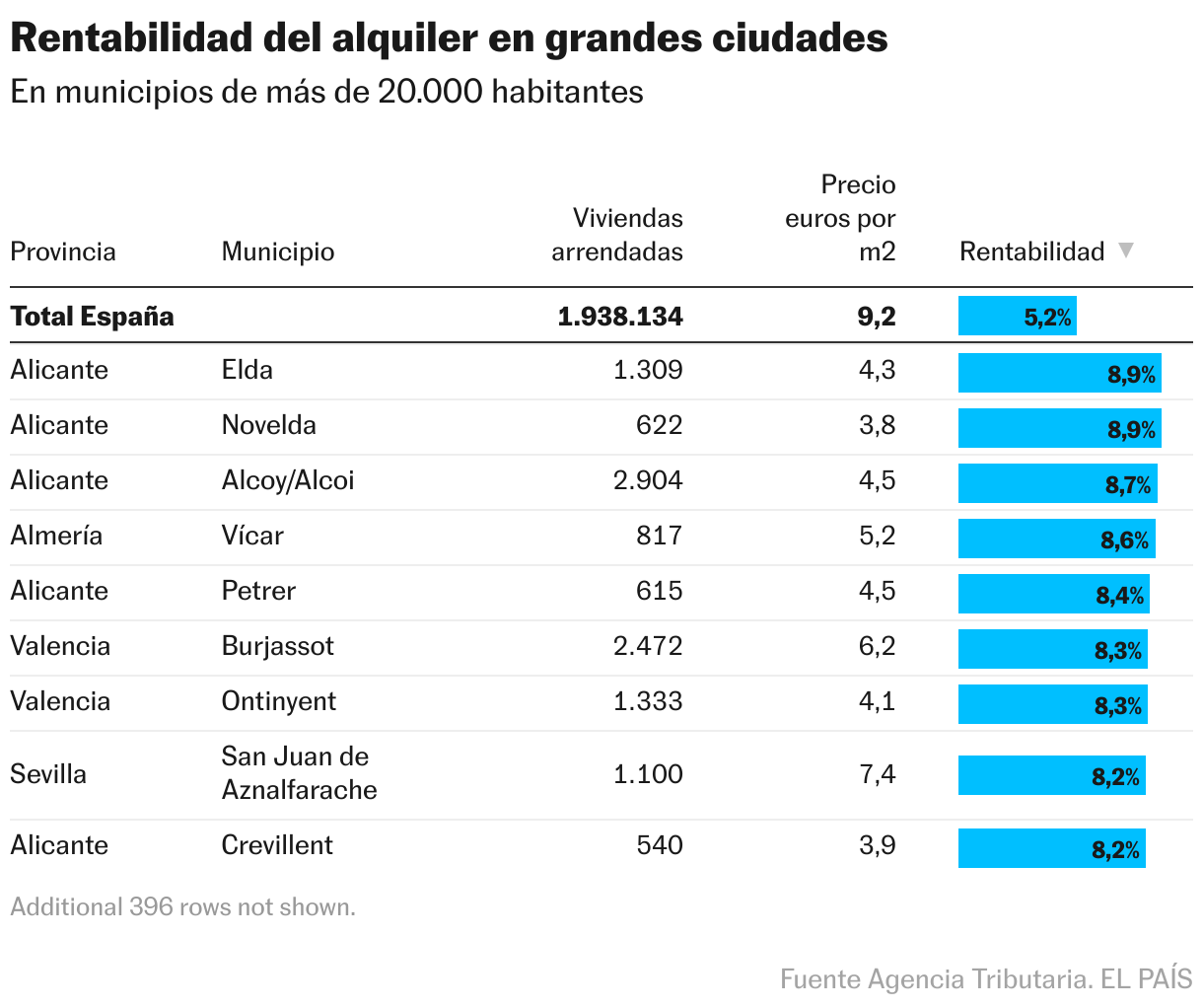

The Tax Agency has published this week, corresponding to the year 2023. In this edition, the farm dependent agency includes a housing centered module that, for the first time, shows variables such as the average income paid per square meter in each postal code of the large cities, the days of effective lease per year or the gross profitability of the rent. One of the conclusions that emerge from these numbers is that gross yields are remarkably higher in peripheral neighborhoods than in the center of the localities.

This profitability difference is mainly explained by the relationship between the acquisition price of housing and the income that can be obtained from it. María Matos, director of Studies and spokesman for Fotocasa, remember that in the central areas the purchase prices have traditionally reached higher levels, which considerably reduces the, despite the fact that the amounts paid by the tenants are greater. In contrast, on the periphery “the initial cost to acquire a house has been more affordable and, although the rentals are lower, the proportion between both factors generates a margin of higher benefit.” The real estate portals have been highlighting this reality and, but now the Tax Agency corroborates it for the first time.

Cities like Madrid illustrate this trend clearly. According to the Treasury data, the highest yields, with profitability of 8% and 7.8%, were registered respectively in the neighborhoods of interruptions and Pavones (both in the district of Puente de Vallecas), two of the humble areas of the capital. High profitability figures were also recorded in several neighborhoods of Villaverde, Carabanchel and Usera. On the contrary, in more wealthy areas of the capital such as Center, Goya, Justice, Recoletos or Almagro – all them in the central almond – the profits were below 4%.

The gross profitability calculated by the Tax Agency is obtained by dividing the average annual rent declared between the cadastral reference value of the property. It is an approximate measure of performance, which does not consider expenses or taxes, and is used to compare geographical areas in a homogeneous way. It refers only to the houses rented by homemade who are natural persons (the owners of houses do not pay IRPF) and leaves out to the Basque and Navarra country, which have their own tax systems.

Although today the profitability is greater in the periphery, that differential is not static. Matos details that in neighborhoods located outside the central ring, as in Madrid beyond the M-30, the rental price has grown up in recent years, “but it still has a margin of travel.” He puts as an example the case of Villaverde, who has seen his profitability duplicate, while other central districts, such as retreat, have shown a slight fall. The logic is clear: “The rental prices in the center seem to have touched the roof, since the rent that a tenant can pay has a limit, while the historically cheaper neighborhoods are still in the expansion phase and have a margin of growth.”

The radiography of this extractivist variable is similar in Barcelona. The city center and, in particular, all neighborhoods that make up L’Eixample record profitability below 3.5%. The highest are given on the periphery, with neighborhoods such as Vallbona, Ciutat Meridiana or Torre Baró (6.8%) at the head. In Valencia, Sevilla, Málaga and Zaragoza the trend is repeated. “The price to acquire housing is cheaper in the peripheries, but with the overheating of the rental market, the landlords also ensure profitability,” says Álvaro Ardura, an urban architect of the Polytechnic University of Madrid. “, So while wages allow it, unless there is a political regulation that ends excessive increases, the trend will continue,” he adds.

Other experts, such as economist Ignacio Ezquiaga, analyze the differences between neighborhoods with some caution. Variations in gross profitability between central and peripheral areas, he explains, can be closer than the aggregate data suggests, especially if the nuances of the calculation are considered. The profitability ratio – mannerly measured as the relationship between the annual income obtained and the value of the property – depends on two variables that do not always reflect the reality exactly: the income for rent and the acquisition price of the house.

On the one hand, the declared annual income may not correspond to the effective occupation of the property, either because it has been empty during part of the year or because there are periods without tenants between contracts, for example. In fact, the Bank of Spain spoke that there could be a cousin to compensate for the greatest risk of default. On the other hand, the value of the housing used as a denominator is usually calculated from market estimates or standard appraisals, and does not necessarily reflect the real price paid by the owner at the time of purchase. This can introduce distortions in the profitability ratio, which could be above what the statistics show, especially in contexts such as the current one, in which many homes were acquired years ago at prices much lower than the current ones.

The data of the Tax Agency go beyond the big cities and show that the dynamics surrounding large cities, as is the case of Toledo, Ávila, Guadalajara or Lleida. In them, the rental price has experienced a significant increase in recent years, driven by the displacement of households expelled from the large capitals, while the purchase prices have not yet followed the same rate of growth.

This situation, says Matos, implies that the gross rentability of rent is momentarily high, as income has been advanced to the increase in the acquisition price. However, this apparent advantage for owners can be temporary. As the real estate market for sale is adjusted and housing prices increase, profitability will tend to balance.