This Thursday, Christmas, is one of the few days of the year that the stock markets in the US and Europe remain closed, excluding weekends. With just two and a half sessions left to close the year, the S&P 500 has appreciated by 16% in 2025, about three points above the average of the last ten years. In Europe, the Spanish stock market leads, with a profitability of 48%, and has once again broken its records for the first time since 2008.

While the leadership of equities in the US remains linked, for the third consecutive year, to the technology sector, the stock market fury in Europe has other tones. Banking and defense have outperformed the market at a feverish pace, even greater than American technology. On the losing side, oil companies and consumer goods manufacturers have fallen behind even inflation.

AI resists the blow

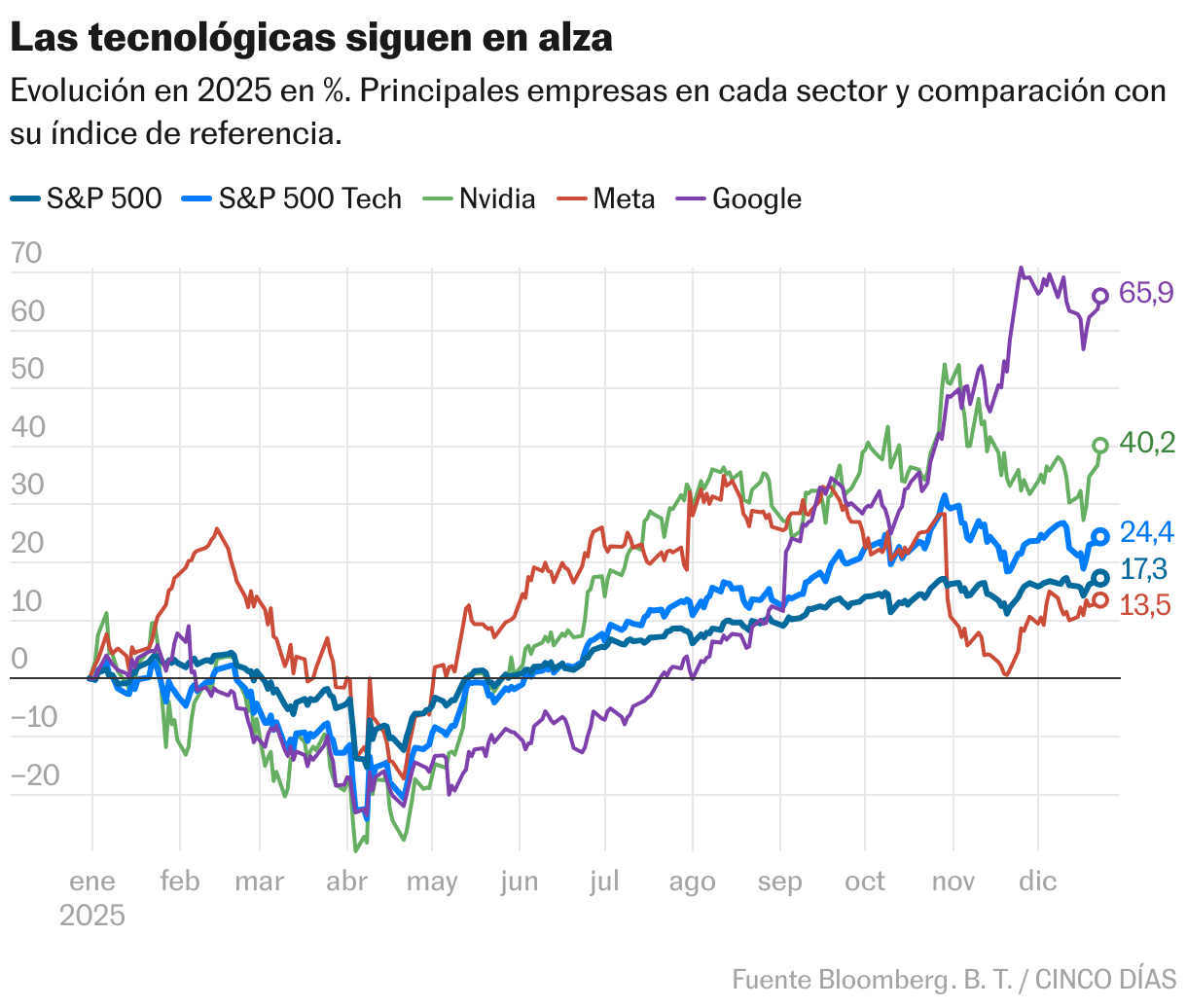

Despite the omnipresence of AI, companies linked to this industry have risen 25% this year, 10 points less than in previous years, with several bumps along the way. Already on January 27, Nvidia’s value in a single session in the history of the US Stock Market – the equivalent of 561,000 million euros -, after the launch of , with its AI model with chips old and cheap.

Although both this company and the rest of the so-called hyperscalers recovered vigorously, since the summer, the market has become more selective, as technology companies have resorted to debt to finance investments in AI with still uncertain future returns. For the first time since the start of the technology race, fund managers say a bubble has formed in the sector, according to a Bank of America survey conducted in November. Thus, investors no longer buy anything with the famous two letters.

Both Nvidia and Meta suffered, after presenting results with strong increases in investment spending. Thus, the manufacturer reduced its growth on the Stock Market from 55% annually to 35%, and the owner of Facebook, from 30% to 15%. Along the same lines, the cloud services provider Oracle, which rose in value by 90% a year, is now advancing 20%. The exception: Alphabet, Google’s parent company, has grown more than 60%, at the expense of Nvidia, after announcing for AI.

Banking is starting to bear fruit

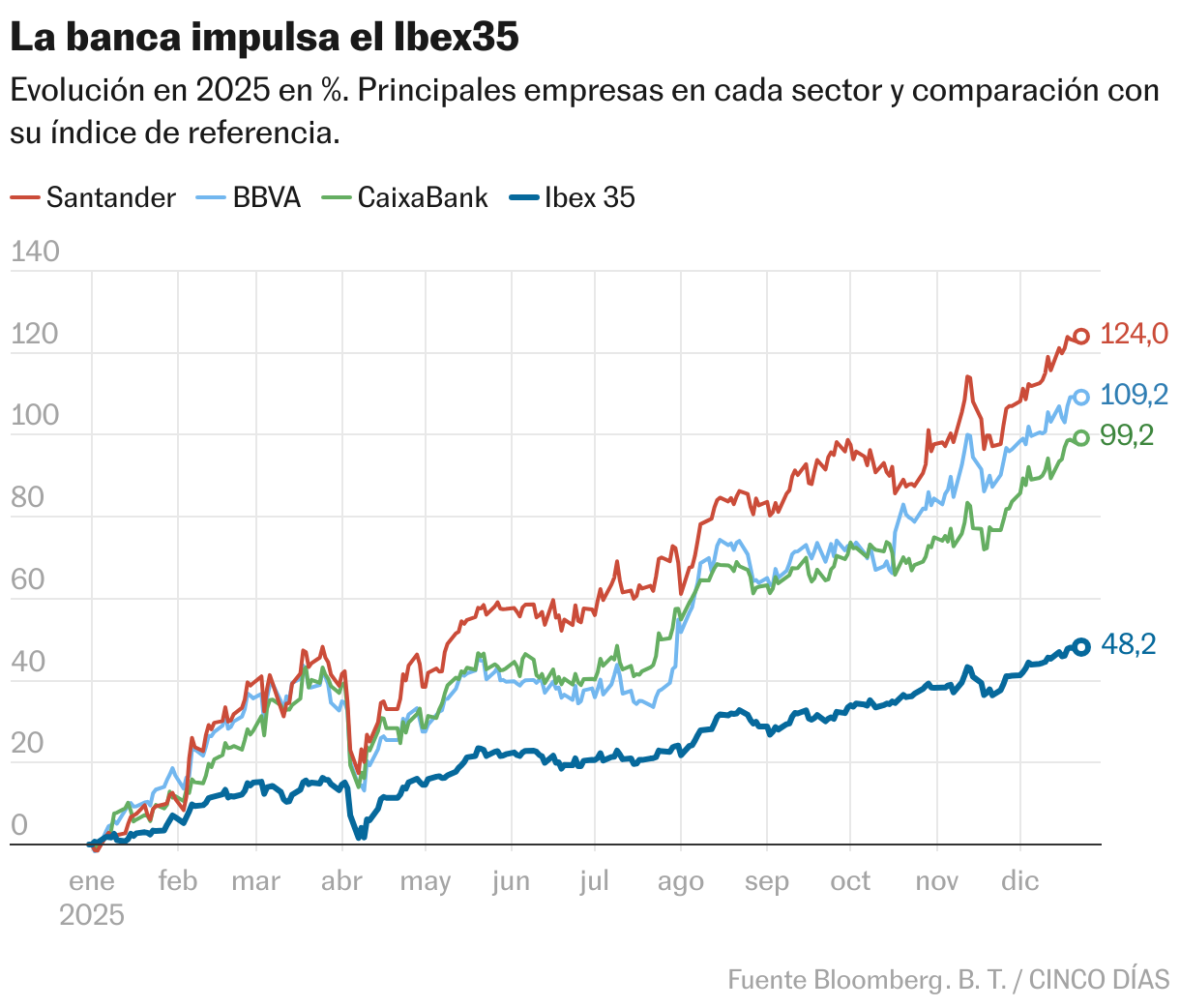

Financial entities have advanced 40% in Europe and have been the main driving force of the Stock Market in Spain. The big three—Santander, BBVA and CaixaBank—have recorded historic highs in profits, which has boosted their shares, with increases in the year of 120%, 110% and 100%, respectively.

“This year has been very good for banks, both in Europe and in the United States, with much more solid balance sheets after years of crisis,” recalled Lucía Gutiérrez-Mellado, Director of Strategy at JP Morgan AM in Spain, to CINCO DÍAS in November. “They have also experienced more attractive types than when they were at zero,” he added, in reference to the pandemic. The good results have allowed the entities to be particularly generous with shareholders, both with dividends of around 4% and with generous share buyback programs in the case of Santander and BBVA. For the Basque bank, it is about: about 4,000 million euros in one go, after the failure of the takeover bid for Sabadell.

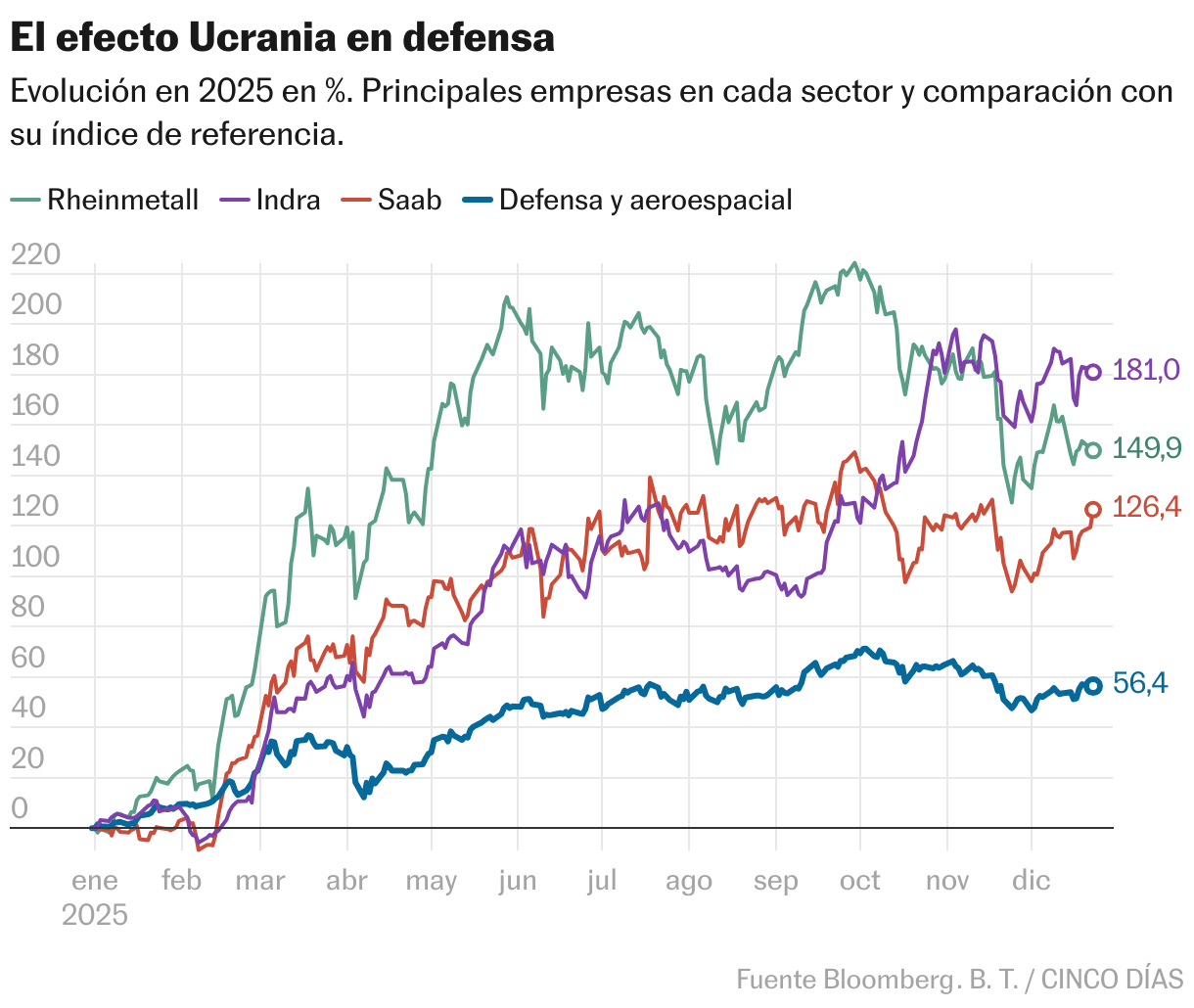

Defense soars with European rearmament

Europe has rearmed itself this year like never before since the war in Ukraine thanks to the push of governments, amid pressure from the United States for greater spending within NATO. The shares of the military industry in Europe have returned an average of 40% a year in the last three years, in the middle of the war in the east of the continent. In 2025, profitability has jumped to 55%.

Trump’s peace plan reached double digits at the end of November, but the sector has rebounded again in December under stock market optimism (linked to geopolitical pessimism) about the long term. “Defense companies had risen quite a bit due to the change in the security situation in Europe and precisely because of these large investment projects for the coming years,” explained Dirk Steffen, Director of Investment at Deutsche Bank in Europe, to CINCO DÍAS at the beginning of the month. So far this year, the Spanish manufacturer Indra has risen 180%, while the German Rheinmetall, 155%, and the Swedish Saab, 120%.

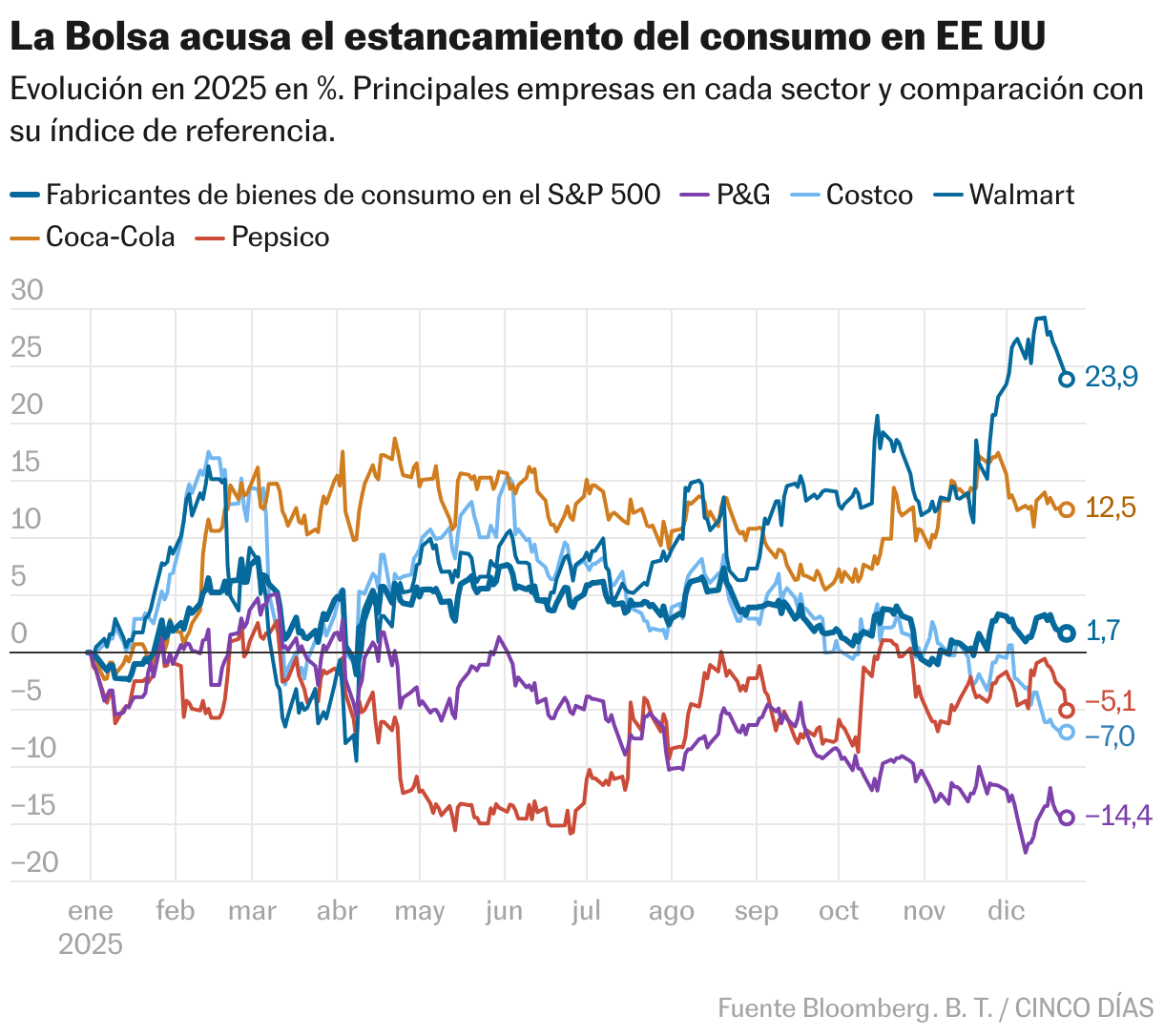

Consumer goods, the canary in the mine

Outside of the glamor of the trading floor, household consumption is the main driver of the economy in the United States. Affected by inflation derived from the tariff war, American families have bought less and less, which has led to stagnation in consumption in September.

The first sector to feel it has been consumer goods manufacturers, which rose just 2%, almost one point below inflation in the US. Among the large companies affected are Procter & Gamble (-15%) and the retailer Costco (-7%). The exceptions are Walmart and Coca Cola, which rose around 25% and 12%, sustained by the strength of their sales.

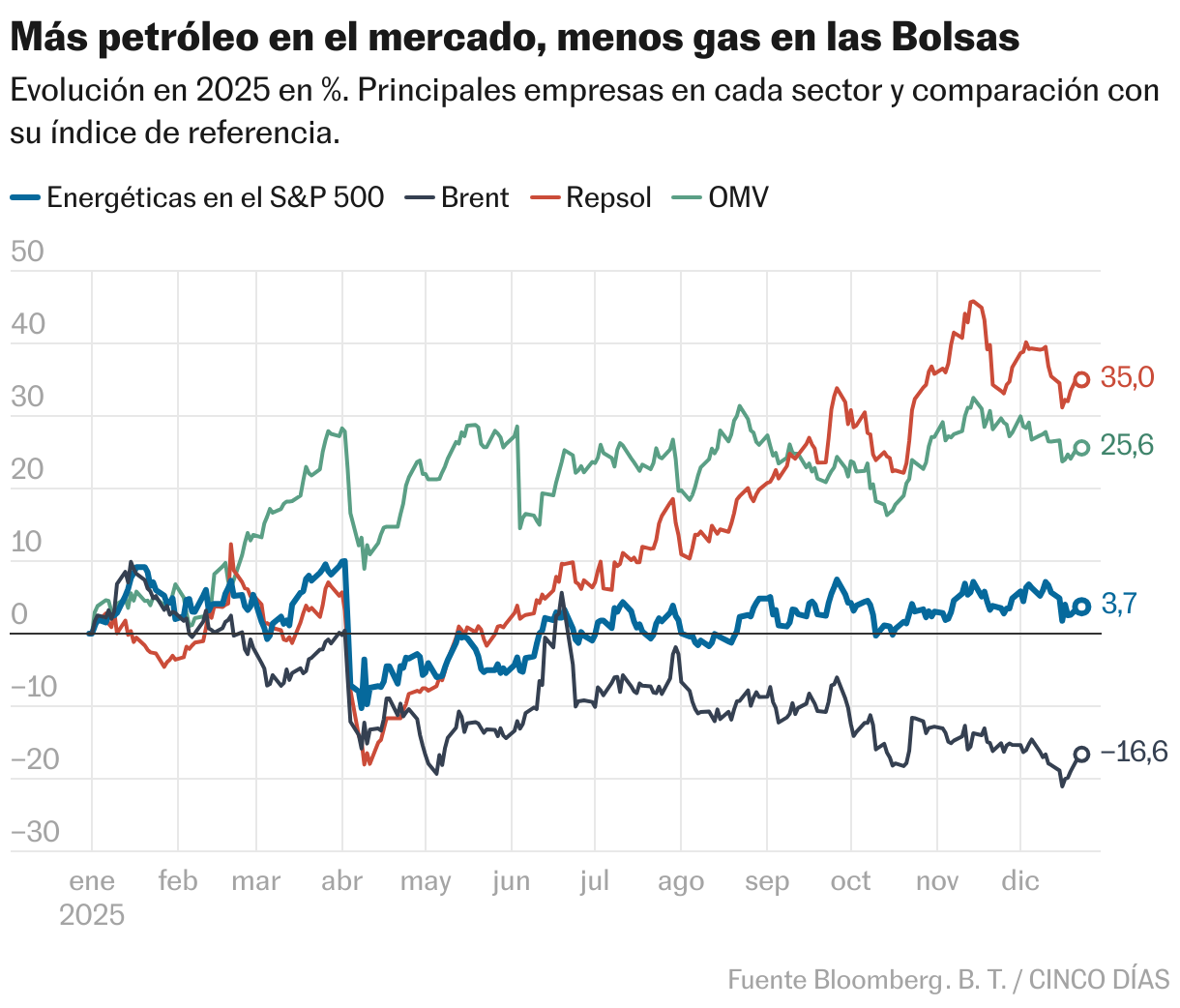

Oil companies lose gas

For years, oil demand has lagged behind production, accelerated not only by the oil cartel (OPEC) but also by other countries, such as the United States, Canada and Brazil. In 2025, of the last four years. “The balances of the world oil market are becoming increasingly unbalanced,” warned the International Energy Agency in a report at the end of November.

Thus, oil and gas producers have yielded barely 2.5% in the US. In Europe, they are resisting with an advance of just over 15%. ExxonMobil and Shell have advanced 10%, while Chevron embitters a year of stagnation. With refining margins above the competition, according to Barclays data, Repsol and the Austrian OMV have maintained a profitability on the Stock Market above 30%.