The Government’s proposal to reform the regional financing system, pending renewal for more than 10 years and whose redesign is devilish because it has to satisfy communities, is part of a forceful change. The Treasury, through several significant tax modifications, intends to shape the number of euros per year to be distributed among the common regime communities, with the aim of rebuilding the battered piggy bank that nourishes them with resources. The immediate result is that practically all territories increase their effective financing in absolute terms. But this seemingly simple photo becomes complicated as soon as we observe in more detail how this increase is distributed and how the relative position of each territory changes.

The Foundation for Applied Economics Studies (Fedea) has unraveled the ins and outs of the reform in a document published this Wednesday by its director, Ángel de la Fuente, one of the greatest experts in regional financing in Spain. The simulation, updated with the latest available data, from 2023, concludes that the changes significantly benefit communities that started from weaker positions in the current system, although not exclusively to them.

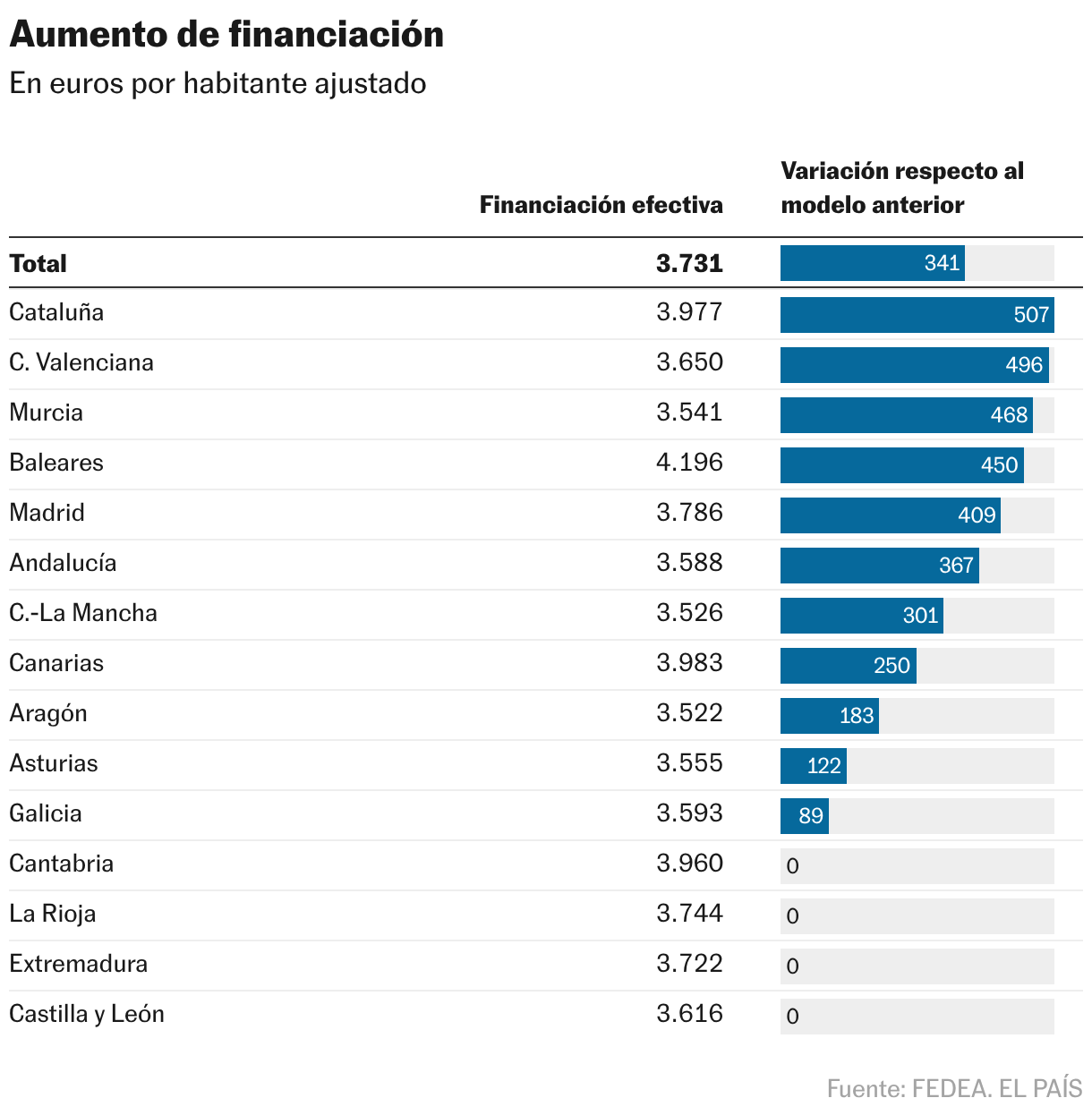

Catalonia is the biggest beneficiary in , with an increase of 507 euros per inhabitant, closely followed by the Valencian Community, which gains 496 euros, and by Murcia, with an additional 468 euros. The Balearic Islands (450 extra euros), Madrid (409 euros), and Andalusia (367 euros) also registered significant increases. It is necessary to speak of adjusted population (a calculation that takes into account insularity, average age, geographical dispersion or orography of the territory) because in this way the inhabitants can be weighted according to their characteristics, which directly influence the cost of public services. If the calculation is carried out without adjusting population, according to Treasury calculations, the biggest beneficiaries are, in this order, Andalusia, Catalonia, the Valencian Community, Madrid and Murcia.

The general increase in resources, a direct effect of the strong financial injection planned, makes it possible to appreciably increase the spending capacity of the majority of the territories. However, not all autonomies participate in the distribution under the same conditions. Some such as Cantabria, La Rioja, Extremadura and Castilla y León – benefited by the current system – do not obtain any profits. The new scheme does not contemplate improvements for them and some compensations designed to avoid nominal losses are pulled out of the hat. According to the Government’s calculations, these compensations will only apply to Cantabria and Extremadura, since Castilla y León and La Rioja would experience a small increase in the volume of their resources.

The picture changes much more profoundly when we move from euros to relative financing per adjusted inhabitant, measured by the traditional 100-based index prepared by Fedea. The scores could change slightly, since the simulation of the study center has not taken into account all the changes foreseen by the new model in the adjustments for adjusted population or the incorporation into the shared wealth tax fund, which does not have a normative collection that is valid as an approximation.

The Valencian Community gains 4.8 points, to 97.8, while Murcia improves by 4.3 points, to 94.9, and Catalonia improves by 4.2 points, to 106.6, which places it above the average. The Balearic Islands and Madrid also improve their relative position, with increases of 2 and 1.9 points respectively. Andalusia’s gain is more moderate, 1.2 points. The rest of the territories lose positions in the table, with impacts of different intensity, but the gap between the best financed and the worst is reduced, from 26.2 points to 18.1.

The effort of the rich autonomies – Madrid, Catalonia and the Balearic Islands – also changes considerably, the three net contributors to the system with both the old and the new model. While that of the first increases slightly, those of the last two decrease substantially.

Criticisms of the plan

De la Fuente explains that, broadly speaking, the pillars of the new model are fairer, with a more equitable distribution of resources and the disappearance of capricious rearrangements. However, there are patches that are introduced specifically to favor the Generalitat of Catalonia, with whom the Government initially negotiated the scheme before presenting it to the rest of the territories.

Fedea, therefore, warns that many of the weaknesses of the proposal are not in the theoretical design of the system, but in the way in which it has been politically realized. The academic recognizes that the core of the model – based on a more homogeneous horizontal leveling and the use of the adjusted population as a central reference – is reasonable and represents an advance with respect to the current system. However, he emphasizes that this core is largely blurred by the final result of the distribution, which incorporates measures for this that alter its internal logic and make it difficult to evaluate the system in terms of equity and efficiency.

The director of the study center refers to instruments such as the Climate Fund or the VAT compensation mechanism for SMEs. They are new adjustments to the distribution that, in his opinion, lack a solid technical basis and do not respond clearly to objective differences in spending needs or to the fiscal capacity of the territories, so, in practice, “they reintroduce the arbitrariness that with good judgment they sought to eliminate.”

Along the same lines, De la Fuente is critical of the use of compensation to maintain the the state in which. Although they may be politically necessary to facilitate the transition to a new model and avoid immediate nominal losses, he points out that they freeze inherited imbalances and reduce incentives to accept future adjustments.

The author also questions whether the sharp increase in resources is accompanied by a real improvement in fiscal governance. The injection of 21,000 million, and “which is presented as a gracious contribution from the central government in order to strengthen the welfare state”, represents an opportunity cost (since it is money that is no longer allocated to other items) and will tend to aggravate the absence of incentives for fiscal discipline. “It would be necessary to make it very visible to citizens that the change implies an increase in the regional tax pressure, or at least the tax pressure for the benefit of the regional governments,” he maintains.

Another element to take into account is that those resources that will pass to the communities will come from the central Administration, which could harm their fiscal consolidation by currently maintaining a considerable structural deficit “compared to the quasi-balance on average of the autonomies.”

At Fedea they are also skeptical about the increase in the personal income tax transfer as the centerpiece of the reform. The author considers that this change is not essential to improve the fairness of the system and adds unnecessary complexity to its architecture. Faced with this option, he defends an alternative approach in which communities can voluntarily decide if they want more resources by adjusting their reference tax rates, so that the cost of that decision is visible to taxpayers.