Top Wall Street bankers during the Trump 2 era have been cautious in approaching political issues, and especially President Donald Trump. The consensus has been: smile and wave, stay in your place, don’t make yourself a target.

But when an “affordability” proposal from Trump earlier this month hit the banks’ profit engine, the mood changed. Publicly and forcefully, Wall Street executives said “no” to Trump.

The situation is not being well received.

On Thursday (22), alleging that the bank improperly closed Trump’s accounts following the invasion of the US Capitol on January 6, 2021. Trump is demanding $5 billion in compensation.

Trump had already threatened to file the lawsuit, which was likely months in the making.

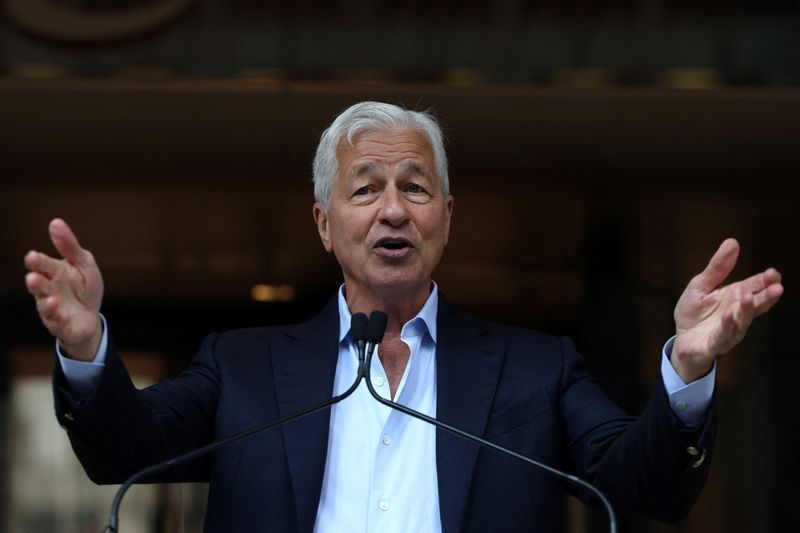

But perhaps not coincidentally, his filing in Florida state court came a day after Dimon told a room full of influential people at the World Economic Forum in Davos, Switzerland, that Trump’s proposal to cut credit card interest rates in half would be “an economic disaster.”

The White House directed questions about the case to Trump’s outside lawyer, Alejandro Brito. His law firm did not immediately respond to a request for comment.

Dimon’s public criticism broke what has become an unofficial, and often uncomfortable, agreement among leaders in corporate America: to stay out of Trump’s way, even when his policies directly affect the bottom line.

When Trump last spring implemented heavy global tariffs that threatened to reduce corporate profits, executives remained silent. The same happened when Trump began attacking the Federal Reserve, an institution whose independence is vital to a stable business environment.

Even when he began explicitly interfering with private companies, and Intel for the government, no one spoke out.

The American corporate world has good reason for its apprehension

Since Trump’s second term began a year ago, he and his administration have investigated, prosecuted or brought charges against a number of perceived enemies, including media companies such as CBS, New York Times e Wall Street Journal.

He threatened Apple with massive tariffs last year over possible disrespect by CEO Tim Cook and CEO Darren Woods during a meeting with oil industry executives earlier this month.

In particular, some trade groups were developing plans to fight back against the Trump administration in defense of their business interests, sources familiar with the matter told CNN International at the time.

However, these plans were shelved as members feared provoking the wrath of the White House.

And CEOs in general are “very alarmed” by the administration’s attack on the Federal Reserve’s independence, according to Jeffrey Sonnenfeld, founder of the Yale Chief Executive Leadership Institute.

Sonnenfeld and his research team discovered that 80% of CEOs surveyed believed Trump was not acting in the best interests of the United States by pressuring Federal Reserve Chairman Jerome Powell to lower interest rates.

It is worth noting that this research was conducted before the Department of Justice began its criminal investigation against the bank and Powell.

The red line

But to Wall Street, the president appears to have finally

In a post on Truth Social on January 9, the president, who is struggling to convince voters that Republicans care about the cost-of-living crisis, said the public will no longer be “exploited” by credit card companies, which charge an average 20% interest rate on card purchases.

While such a limit would likely need to come from Congress, the statement rattled Wall Street, provoking rare public criticism from executives.

“A rate cap is not something we can support,” Citigroup CEO Jane Fraser said during the bank’s earnings call.

Bank of America CEO Brian Moynihan – already accustomed to being publicly reprimanded by Trump – said last week that a limit would not have the effect Trump seeks: “If you reduce limits, you will tighten credit, meaning fewer people will get credit cards and the limit available on those cards will also be restricted.”

But Dimon’s declaration of “economic disaster” at Davos was a more direct criticism, coming from Wall Street’s most prominent figure, and someone who has had a troubled personal relationship with Trump.

Trump x Dimon

Trump and Dimon have had a difficult relationship for years.

In 2018, in a comment that Dimon almost immediately walked back, the Wall Street titan told a panel at the bank’s headquarters that he “could beat Trump” in a head-to-head presidential contest “because I’m as tough as he is, I’m smarter than him.”

Trump responded online, calling Dimon “a terrible speaker and nervous.”

Dimon’s approach toward the president during his second term has been much more moderate.

In his Davos interview, Dimon said he disagreed with some of Trump’s policies, agreed with others, but largely avoided a question about why he and other CEOs have been so reluctant to stand up to the president.

He may have seen what was coming

After a measured statement during JPMorgan’s earnings call in which he disagreed with Trump’s plan for credit card fees (“it would be dramatic for the subprime“) and his criminal investigation against Powell (“not a good idea”), Trump publicly criticized Dimon.

“Jamie Dimon probably wants higher rates,” Trump said on January 15. “Maybe he’ll make more money that way.”

Two days later, after the Wall Street Journal reveal that Trump announced he would sue.

“There has never been such an offer, and in fact, I will be suing JPMorgan Chase in the next two weeks for incorrectly and inappropriately decertifying me following the January 6th Protest,” Trump said on Truth Social.

CNN International’s Matt Egan, Chris Isidore and Phil Mattingly contributed to this report.