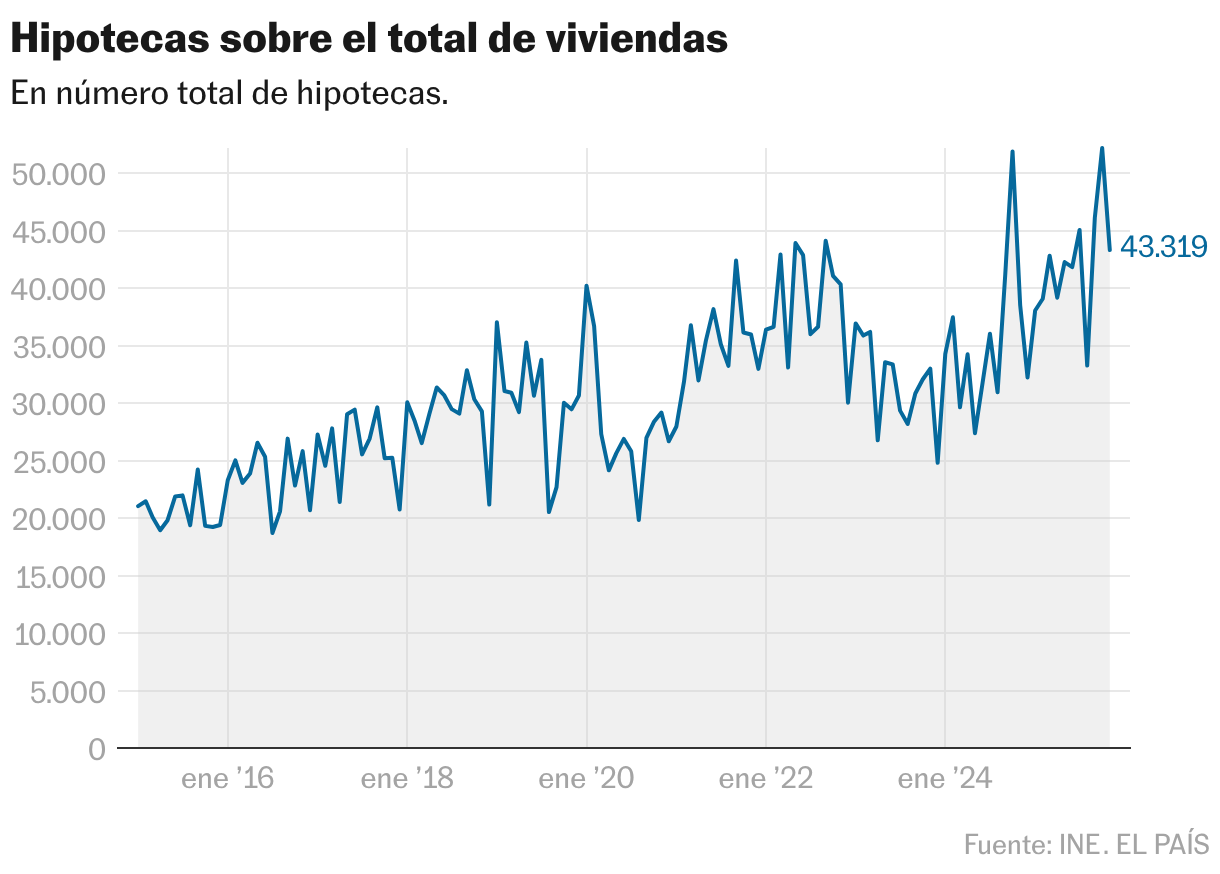

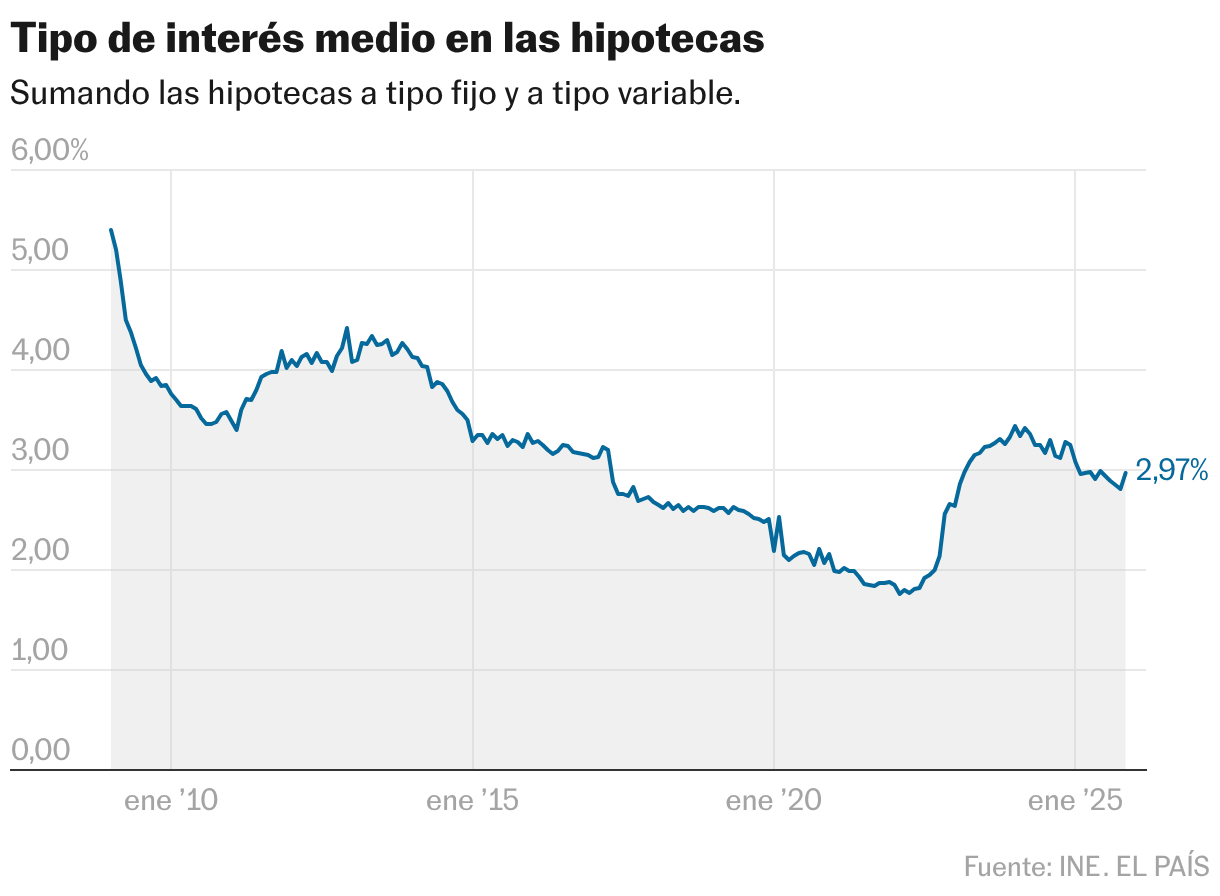

Just a week ago, the National Institute of Statistics (INE) published the total number of purchase and sale operations that were closed. The sum was lower than that of October, but it was well above the records obtained in the same month of 2024. This Monday, the statistical office reported the total number of mortgages that were signed last month, and (as expected) the relationship is similar: 43,319 loans were agreed, 17% less than in October, although these represent 12.4% than in the previous month of November. The average amount of mortgages was 170,771 euros, slightly higher in the monthly comparison (2.2%), although much higher than 12 months ago (+11.7%); while the average interest rate stood at 2.97%, 5.8% higher than in October, but considerably more accessible than in the eleventh month of 2024 (-9%).

The mortgage firm in November did not improve its October results (52,198), but its data was the highest for this time of year in more than a decade. Only the 43,797 operations that were signed in 2010 exceed (narrowly) the 43,319 in 2025. The improvement experienced in the volume of loans is 12.4% higher compared to the data from November 2024, and represents the second consecutive month in which more loans are signed than in the same period of the previous year.

“We continue to have the best November in the last 15 years and, most importantly, we maintain a clearly growing trend,” celebrates Ricard Garriga, CEO of Trioteca. “If we compare the first eleven months of 2025 with the same period of the previous year, the accumulated increase in mortgages is 17.9%,” he points out. In round numbers, between January and November 2025, 463,232 loans have been signed, a figure that exceeds those that were granted in all of 2025: 425,522.

Taking this result as a reference, in the first eleven months of 2025, 2,005 operations have been signed per business day, while in 2024 as a whole the average was 1,687. “We are talking about an increase of more than 18% in the number of daily mortgages. These levels, around 2,000 operations per day, have not been seen since 2010,” explains Garriga.

However, comparisons with that year, just after the bubble burst, are delicate. “We take 2010 as a reference, but we are still far from that year, when more than 2,400 mortgages were signed daily and more than 600,000 were signed for the entire year.” In this sense, he adds that “everything indicates that 2025 will close above 500,000 mortgages, a very relevant figure that confirms the strength of the current market.”

November has been a small blip that, however, does not cloud the record forecasts. By territory, the falls in absolute terms of the Community of Madrid (-2,060) and Catalonia (1,652); and percentages of Extremadura (-33.8%) and the Balearic Islands (-28.4%) ―leaving aside the autonomous cities of Ceuta and Melilla, with higher percentages, but less representative due to their volume―, have weighed down the overall result for November. Only the Basque Country (83), Cantabria (54) and Ceuta (24) show a positive balance in terms of loans signed in the eleventh month of the year compared to the October figure.

Same type, more quantity

Although the dynamism in the volume of contract signing is due, among other reasons, to the stability of interest rates – the average rate in November was 2.97%, and has continued to remain below 3% since January – the average amount of mortgages maintains its upward progression in the final stages of the year. The 170,771 euros in November are the second highest figure of the year (in September it rose to 171,612 euros), and represent 18,538 euros more than in January. “According to the INE, the average Spaniard is signing fixed mortgages at around 2.94%, while the average mortgage signed through Trioteca is 2.23%. This represents a saving of 71 basis points,” highlights Garriga, also co-founder of the Spanish Association of Mortgage Brokers (AEBH).

As has been happening throughout the year, the majority option continues to be the fixed rate mortgage, above the variable rate. In November, 61.5% of the first modality were signed, and 38.5% of the second. These are results practically identical to those of October. “Today, the fixed mortgage is the majority option and the variable has practically disappeared from the radar of the average buyer,” recalls Garriga.