In a radical revision of its estimates, after the almost complete stoppage of stoz navigation on Sunday, March 1st. An event without historical precedent in modern times, as reported by JP Morgan.

The key assumption by U.S. bank analysts that an unprecedented disruption would remain unlikely “collapsed,” it said, forcing markets to reassess geopolitical risk and the resilience of global energy trade.

The shutdown followed the large-scale joint US-Israeli military operation against Iran, which the US president presented as a move aimed not only at weakening Tehran’s military capabilities but also at creating the conditions for a political upheaval.

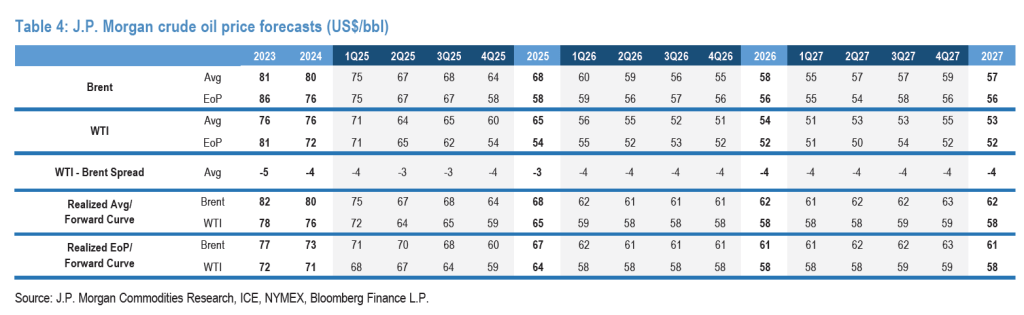

JP Morgan now expects an immediate repricing of geopolitical risk. Brent is expected to move from Friday’s (27/27) $73 to the $80-$85/barrel range, with the entire contract curve shifting upward and backwardation strengthening significantly, reflecting increased risk to short-term supply.

The four critical variables for the course of oil

Beyond the initial “reflexive” reaction, JP Morgan emphasizes that price action will depend on four key factors:

- How many barrels will naturally be disturbed

- How long will the outage last?

- If reliable alternative sources of supply (including strategic stocks) can be activated.

- What will be the next phase of the crisis?

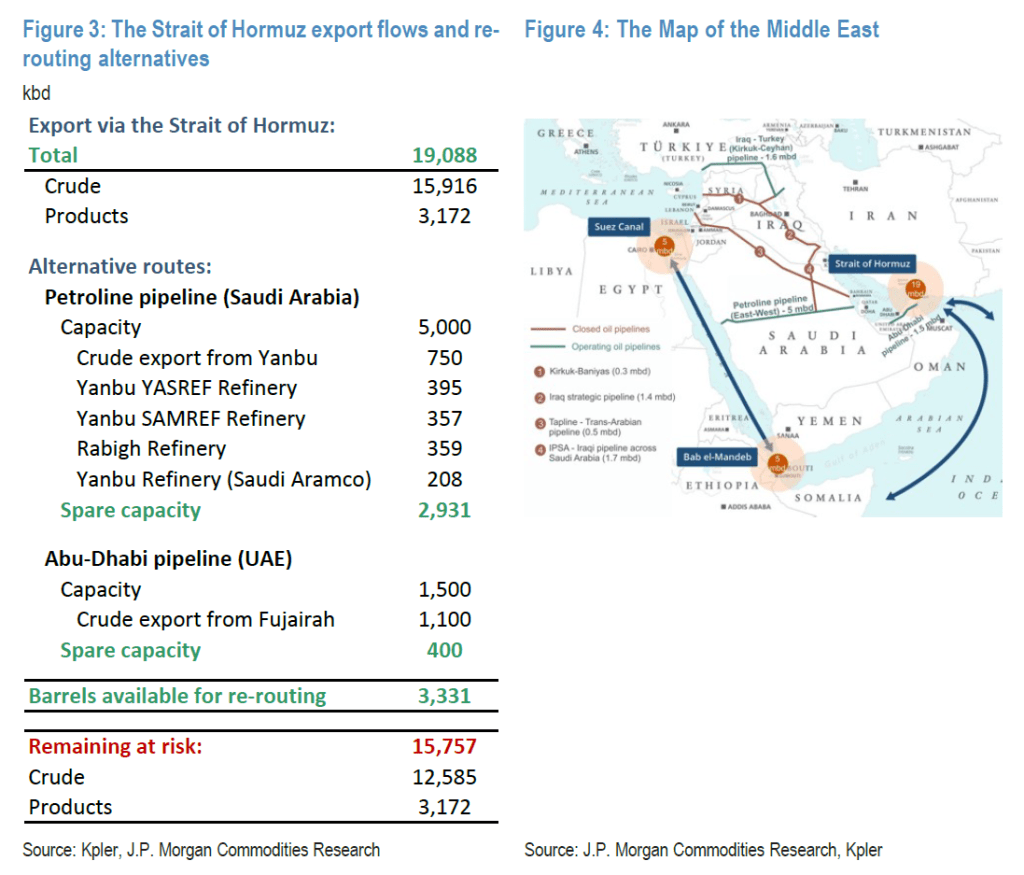

So far, Iran has avoided hitting major oil infrastructure, focusing on military and strategic targets. Although the passage of tankers through the Strait is almost nil, the reason is mainly preventive. Insurance companies canceled or increased war risk insurance, while shipping giants such as Maersk, Hapag-Lloyd, CMA CGM and MSC suspended transits or cargo bookings to the Middle East.

of which 16 million barrels of crude, usually pass through the Strait. Available bypass pipelines in Saudi Arabia and the UAE can divert just 3.3 million barrels, leaving nearly 15.8 million barrels without an alternative route in the event of a complete shutdown.

JP Morgan estimates that Gulf producers can sustain production for about 25 days, using storage and available tankers. Beyond this interval, they will be forced into mandatory production cuts.

Scenarios and implications for supply

The duration of the military operation remains uncertain. The operational plan calls for at least five days of bombing, with the US president leaving open the possibility of either a rapid de-escalation or a prolonged engagement.

At the same time, JP Morgan points out that although the market entered the crisis with a surplus of about 1.4 million barrels per day, a prolonged outage of more than 25 days could remove up to 16 million barrels per day of exports, an amount that far exceeds available spare capacity outside the Persian Gulf.

U.S. shale oil production could increase, but it takes months to materialize. Russia may add 0.3–0.4 million barrels per day, but this contribution is considered marginal in relation to potential losses. Thus, a prolonged disturbance could quickly turn a surplus into a severe structural deficit.

The risk of destabilization and historical examples

JP Morgan believes that the US-Israel strategic objective may not be to completely overthrow the regime, but to change its behavior, along the lines of the pressure exerted on Venezuela. However, the main risk remains institutional collapse and a possible civil war scenario, given the intense internal polarization in Iran.

Historically, there have been eight major regime changes in medium and large oil-producing countries since 1979, with an average increase in oil prices of 76% from the start to the peak of the crisis. In the first month, prices rose by around 5%, while on a three-month horizon the increase reached an average of 30%, with supply losses intensifying mainly in the six months.

Overall, however, he cautions that the duration of the crisis and the degree of supply disruption will determine whether the current shock turns out to be temporary or the start of a new, highly inflationary energy phase for the global economy.

Source: