Is it possible to retire early? It is the million-dollar question that many workers ask themselves. The answer is yes, but it is a decision that should be weighed very carefully (and with a calculator at your side). Among the issues to always keep in mind, a priority is to get an idea of . Another is to be aware of how long you have been contributing (to know at what legal age it is possible to retire, whether at 65 years of age, or later). If the necessary requirements are met, a worker can advance his retirement to age 63, 61, or even earlier. But it has a price: a smaller pension.

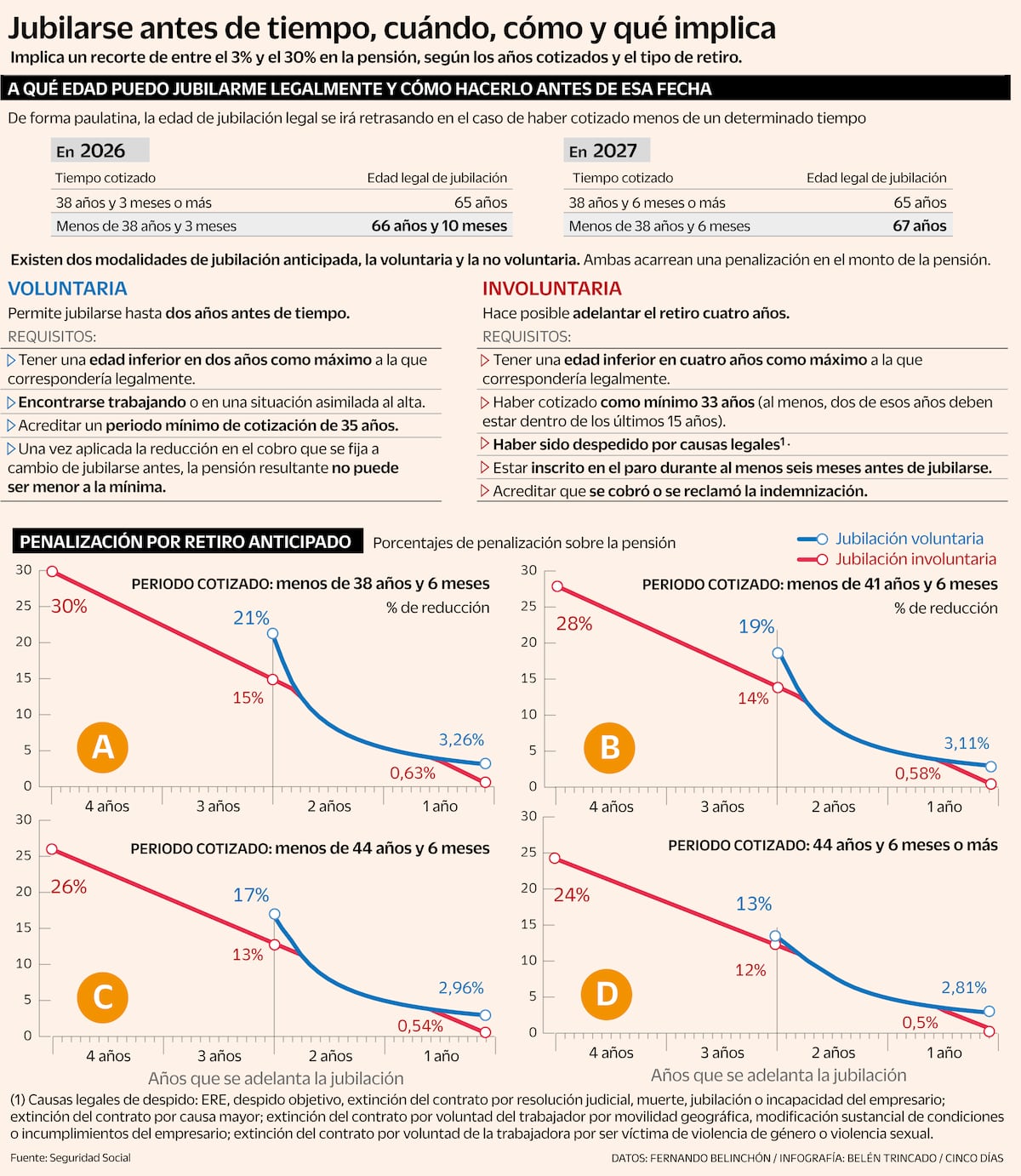

As a consequence of the reform of the pension system approved in 2011 by the Government of José Luis Rodríguez Zapatero, year after year, the legal retirement age has been gradually delayed depending on whether contributions have been made for a certain period of time or not. In 2027, when this reform is fully implemented, the legal retirement age in Spain will be 67 years for those who have contributed less than 38 years and 6 months. If you have contributed for more than that time (which implies having worked continuously since the age of 26), the legal age would continue to be 65 years. This 2026, the legal retirement age if 38 years and 3 months of contribution time is not exceeded is 66 years and 10 months, if that contribution period is exceeded, it is 65 years.

Now, whether the time limit that allows early retirement is not reached or exceeded, retirement can be accelerated. There are several ways to retire before the established legal age, although, generally, there are four: a pre-retirement agreement with the company you work for, request voluntary early retirement, be able to invoke what is known as non-voluntary early retirement, or take advantage of one of the exceptions contemplated by the regulations.

Is early retirement the same as early retirement?

No. For the purposes of the retired person, the two things are very similar, but the first, early retirement, far from being a right, is a negotiation with the company for which one works that involves a disbursement for the company. In this sense, it is more similar to an agreed dismissal, and for this reason it is only offered to workers with high seniority. Thus, and by agreement between the two parties, the company stops paying the monthly salary and, in exchange, assumes a lower monthly payment and is responsible for Social Security contributions until the legal retirement age.

An example. In the case of Telefónica, in its last exit plan it agreed to a . To encourage voluntary departures, the telecom offered that it contemplates that those born between 1969 and 1971 who offer to leave will receive 68% of the regulatory salary until the age of 63 and 38% thereafter. For the period from 1965 to 1968, the income will be 62% until age 63 and 34% afterward; while for those born in 1964 or before, the percentages will be 52% and 35%, respectively. The employee stops working, but it is the company that pays and decides how much it will charge through negotiation.

Unlike the fundamental role that negotiation with the company plays in early retirement, however, in early retirement it is Social Security that assumes the payment because one has already retired officially and all active workers have the right to benefit from it when the requirements are met.

Within early retirement there are two categories: voluntary and involuntary or non-voluntary. Each one has its own characteristics and requirements, but both imply a penalty in the amount of the pension that will be received throughout retirement and follow the same application process. The cool part is that in exchange for retiring earlier, you will receive less pension for the rest of your life.

Voluntary early retirement

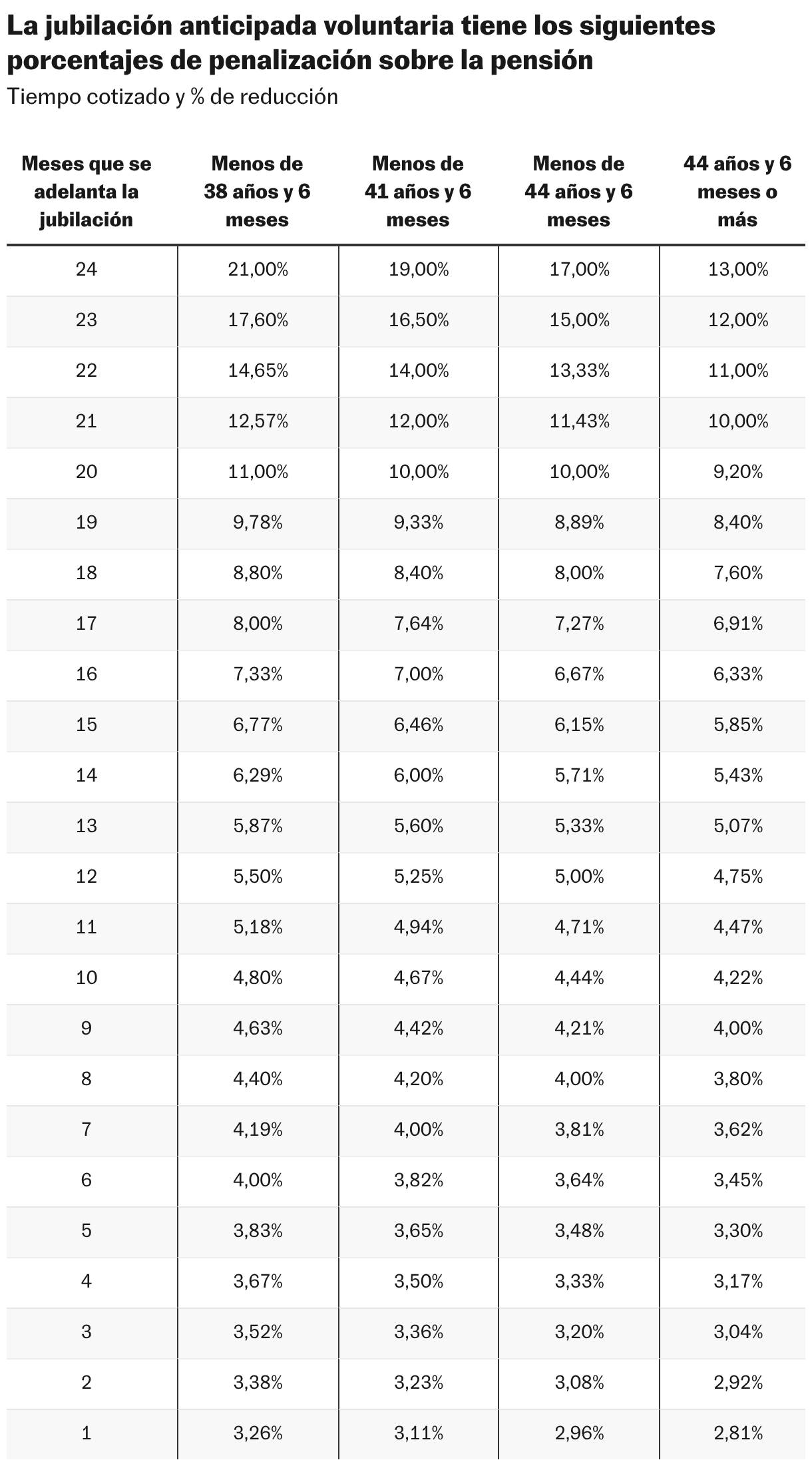

In the case of volunteering, the worker himself is the one who, while still active, asks to retire early. You do not need approval from your company and this allows you to advance the age that would legally correspond by a maximum of two years. In order to request it, it is necessary to have contributed for at least 35 years, but it has penalties in the form of a lower pension. That depends on how far in advance it is requested and the time quoted. Logically, retiring earlier penalizes and so does having contributed for less time.

An example. There is a worker who has contributed for 36 years and decides to request voluntary advance payment. He requests it as soon as possible, that is, with two years left before his legal retirement age. This worker will receive 21% less than what he would have had if he had waited two more years to retire, since the penalties are designed to be especially severe at the beginning. If this same worker waits only five more months and decides to request early retirement with 19 months left before his or her retirement age, the penalty would be 9.78%. The following graph shows how the different penalties vary depending on the time quoted and how early it is requested.

As when calculating the amount of the pension, the time contributed is a very important variable to know how much the retirement can be anticipated. The worker in the previous example, having contributed for 36 years, should in theory wait until he turns 66 years and 10 months to retire, having the possibility of bringing it forward at most to 64 years and 10 months at the cost of bearing a penalty of 21% on the pension that in theory he would be entitled to receive if he waited until the legal age. If that same worker had contributed for more than 38 years and 3 months, his legal retirement age would be 65 years, and he would then have the potential to retire at age 63 if he assumes the maximum penalty of 21% on his pension. Time, money, being able to stop working… When requesting voluntary early retirement, everything must be put on a balance that, depending on what is valued more, will end up leaning one way or the other.

Involuntary early retirement

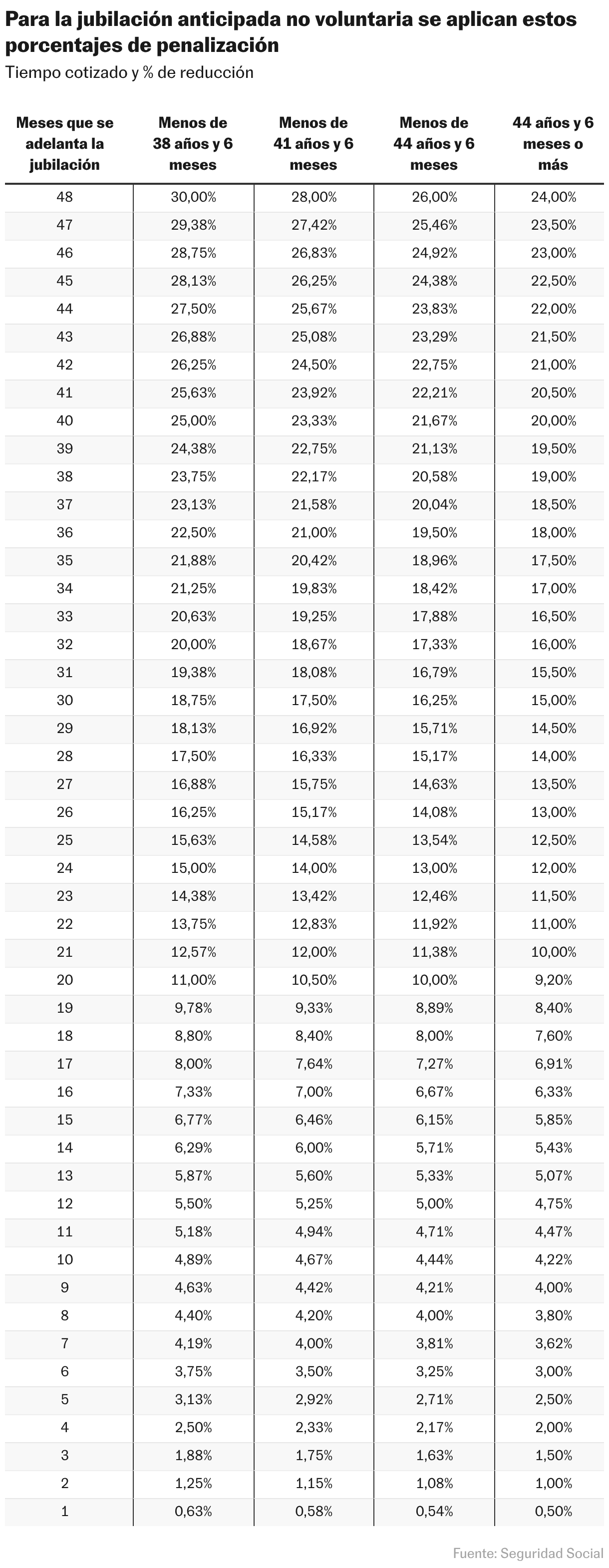

Involuntary early retirement is a type of retirement that can be requested if you become unemployed when you are close to the legal retirement age. Through it, it is possible to retire up to four years before the corresponding legal age. This implies, in the case of having a working life with a contribution period of more than 38 years and 3 months upon turning 61, being able to retire at that time.

To benefit from it, it is necessary to have contributed for at least 33 years and, at least, that two of those years of contributions fall within the last 15 years of working life before requesting it. It is necessary to have received unemployment benefits for at least six months before applying for it and Social Security allows it to be applied only in the case of having been fired for legal reasons.

Among the legal causes are having been affected by an ERE, having been subject to objective dismissal (that is, for reasons beyond the control of the employee) or a termination of the contract by judicial resolution (due to a serious breach of contract by the employer that has been recognized by a judge). Also having lost the position due to death, retirement or disability of the individual entrepreneur who was the employer or after a termination of the contract due to force majeure (for example, a fire or a flood).

The termination of the contract at the will of the worker is also considered a legal cause, but only if it has been due to geographical mobility, a substantial modification of working conditions or due to non-compliance by the employer. Furthermore, the termination of the contract at the will of the worker due to being a victim of gender violence or sexual violence also gives rise to this type of retirement.

Again, following the same logic as in the case of the volunteer, the penalty is greater the sooner it is requested. Also, if it has been quoted less. The following graph breaks down in detail the percentage reduction applied to the pension.

Exceptions contemplated by the standard

There are two main types of exceptions. Those of personal circumstances and those that establish specific rules for certain types of professions that have subsidized retirement and allow professionals in the sector to retire earlier.

People with a degree of disability equal to or greater than 65% will be able to retire early without affecting the total amount of their pension. That is, without being affected by the reducing coefficients set out above. Furthermore, instead of being guided by the rules that allow retirement to be advanced only two or four years (depending on whether it is voluntary or involuntary, respectively) before the legal retirement age, by calculating that they are applied to the total time worked, the retirement pension can be accessed as soon as 52 years of age. , people with a degree of disability equal to or greater than 45% could also opt for this modality.

On the side of subsidized professions, early retirement is contemplated for each of the following cases. Workers in the mining sector, professionals in the railway sector, workers in the airline sector (except cabin crew), workers of the Special Regime for Sea Workers, firefighters, local police, members of the Ertzaintza, the Mossos d’escuadra or the regional police of Navarra.

Artists are also included in the special regime. For example, singers, dancers and trapeze artists may receive a retirement pension from the age of 60, without the application of reducing coefficients, when they have worked in the specialty for a minimum of 8 years during the 21 years prior to retirement. Likewise, bullfighting professionals have a bonus regime. Bullfighters can retire at the age of 55, as can rejoneadores, novilleros, banderilleros, picadors and comic bullfighters, as long as they prove that they are registered or in a situation similar to that of registered on the date of the causative event and have performed in a certain number of bullfighting shows.

Another special group for retirement is the military. At 45 years of age, members of the army and sailors are forced to retire. These professionals only have the option of continuing in the army if they pass a selective testing process known as access to permanent troops. If this process is not passed, forcibly retired military personnel who wish to do so and have served for at least 18 years become part of the special availability reserve, where they can continue to be mobilized if necessary.

The collection of the pension of 704 gross euros per month that retired military personnel can access at the age of 45 is linked to that condition of being. The military receives it until the age of 65 and, although it is incompatible with receiving any other public salary, it is compatible with unemployment benefits and with income from the private sector.

Finally, thanks to a law approved by Felipe González, all former presidents of the Government have a lifetime pension compatible with any other type of payment that amounts to 79,336 gross euros per year.

What happens if I am self-employed and want to retire before the ordinary age?

Self-employed workers have a more restricted regime than those who are employed. The self-employed cannot access involuntary early retirement, but they can access voluntary early retirement following the same requirements and penalties. Exceptionally, if the requirements are met, they can also retire early under the same conditions as employed workers if they have contributed long enough in one of the professions that have a special regime.

Early retirement applications, for both self-employed and employed workers, can be submitted through , or through , which includes instructions for correct completion. In case of doubts, the official staff of the attention and information centers can provide the advice and help necessary throughout the process. To receive this assistance, you can request an appointment or by calling 901 10 65 70 and 915 41 25 30.