Between 2014 and 2024, the top 10 sports properties increased the global value of their media rights by 113%, from approximately $15 billion to $32 billion. In the same period, the next 20 properties grew from around US$5 billion to US$7 billion, an increase of 40%.

The data, released by the Boston Consulting Group at the beginning of the month, shows that the value is increasingly concentrated in a restricted group of leagues and competitions with global reach. The leaders grew almost three times faster and are now worth, together, four times the next block.

The numbers support Michael Broughton’s thesis about the state of sports media. The analysis he made at the beginning of the year came from a specific context: the fall of cable TV, the collapse of regional sports channels and the uncertain future of Warner Bros amid the dispute over Netflix and Paramount.

Continues after advertising

In Broughton’s view, cord-cutting was never the secret villain. Reports already showed the movement in 2014, recalls the analyst. The real problem was something else: the belief that it would be possible to execute a classic deleveraging strategy on an asset whose revenue was slowly shrinking while the cost of rights continued to inflate.

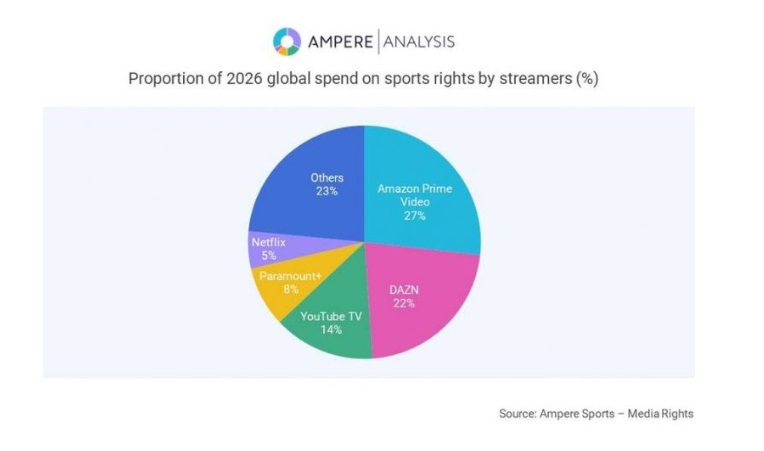

It is in this environment of rising costs and falling traditional revenues that Ampere Analysis’ new numbers gain relevance. Released on February 2, the data shows the advance of streaming platforms over the territory previously dominated by linear broadcasters, and reveals an asymmetry that could redefine negotiating power from now on.

Streaming players are expected to spend US$14.2 billion on sports rights in 2026, up 7% from the US$13.2 billion forecast for 2025.

Continues after advertising

The most relevant data, in turn, is not the absolute growth, but the composition. According to Ampere, 44% of spending will come from generalist platforms, those whose main focus is not sport.

“The growing importance of live sport in driving subscriber acquisition and retention, as well as maximizing advertising revenue, has led generalist services like Amazon Prime Video to become increasingly active in purchasing rights,” said Danni Moore of Ampere Analysis.

The Unofficial Partner podcast was the one who warned about the detail that goes unnoticed, drawing attention to three factors that relativize the headline.

Continues after advertising

First, streamers are taking a bigger share of a stagnant market. The 7% growth suggests maturation, not explosion.

Second, the comparison between streamers and traditional broadcasters is inherently unfair. Digital platforms operate globally; linear broadcasters operate in delimited territories. The addressable market is different.

Lastly, the very definition of “streaming service” is becoming fuzzy. DAZN began operating linear channels via satellite and cable. ESPN is classified as a sports division that integrates linear TV and streaming. Convergence is a fact.

Continues after advertising

“Calling DAZN a pure streaming service may no longer reflect reality. It may be a company that prioritizes streaming, but is not limited to it,” said Yannick Ramcke at Unofficial Partner.

The pure model test

DAZN’s trajectory summarizes the fragility of the pure model. Analyst Simon Lane questions the viability of global sports streaming in its original form. The company is approaching profitability, but has spent US$6.7 billion in the process, acquired Foxtel, a profitable cable TV operation, and left or is trying to leave markets where it has not achieved sufficient scale, such as Ligue 1 and the Belgian league.

Recently, Nick Meacham also analyzed this inflection. DAZN, remembers the CEO of SportsPro Media, was for almost a decade the perfect example of the “scale first, worry later” strategy. Lose money. Buy rights. Grow subscribers. Repeat.

Continues after advertising

The scenario, however, changed. Financial discipline replaced expansion at any cost, while valuations fell. In Meacham’s view, overly subscription-dependent models began to appear fragile.

And this leads to the question posed by Yannick: the subscriber retention thesis loses strength when the cost of acquiring a new user exceeds the value he brings. “Forget about retention,” he said. “That’s not the goal. It’s just attracting a new subscriber to the ecosystem, and that’s expensive.”

The asymmetry that defines the game

The question that Unofficial Partner places at the center of the debate is the most uncomfortable for rights holders: what happens when generalist platforms stop buying?

Purely sporting services need sport to exist. Generalist platforms do not. They can simply reallocate capital to other entertainment verticals.

The US$14.2 billion projected for 2026 largely reflects acquisition strategies in mature markets. But ROI calculations are changing. If Amazon, Netflix, or Paramount conclude that the incremental cost of acquisition exceeds the value generated, competitive pressure eases. And without this, the pricing power of rights holders weakens.

According to Unofficial Partner, advertising inflation has become the last relevant margin. After two years of aggressive readjustments, subscriptions have reached natural limits. Licensed products, betting and fantasy did not scale as expected. Inventory within broadcasts can generate up to 20% additional value without the need for new rights.

The promise of direct sales to consumers comes up against reality. Even successful services focused on a single sport face the need to multiply their subscriber base three or four times to replace traditional licensing revenues.

The future, Unofficial Partner suggests, tends less towards a “Netflix of sports” and more towards the incorporation of sport into broad entertainment platforms, essentially pay TV distributed over the internet.

This reading is in line with Colin McRae’s analysis: platforms stopped optimizing just for advertising insertions and started targeting habits. The logic is no longer to sell one-off exposure, but to build recurrence and behavior.

“The attention gained accumulates, crosses screens and anchors itself in fan communities.”, he wrote.

In sport, this creates an advantage for generalist platforms. They can give up, but exclusively sports services cannot.

Paraphrasing the Unofficial Partnerthis asymmetry unbalances negotiating power, transferring it from rights holders to platforms. And it reverses decades of competitive dynamics that fueled entitlement inflation.