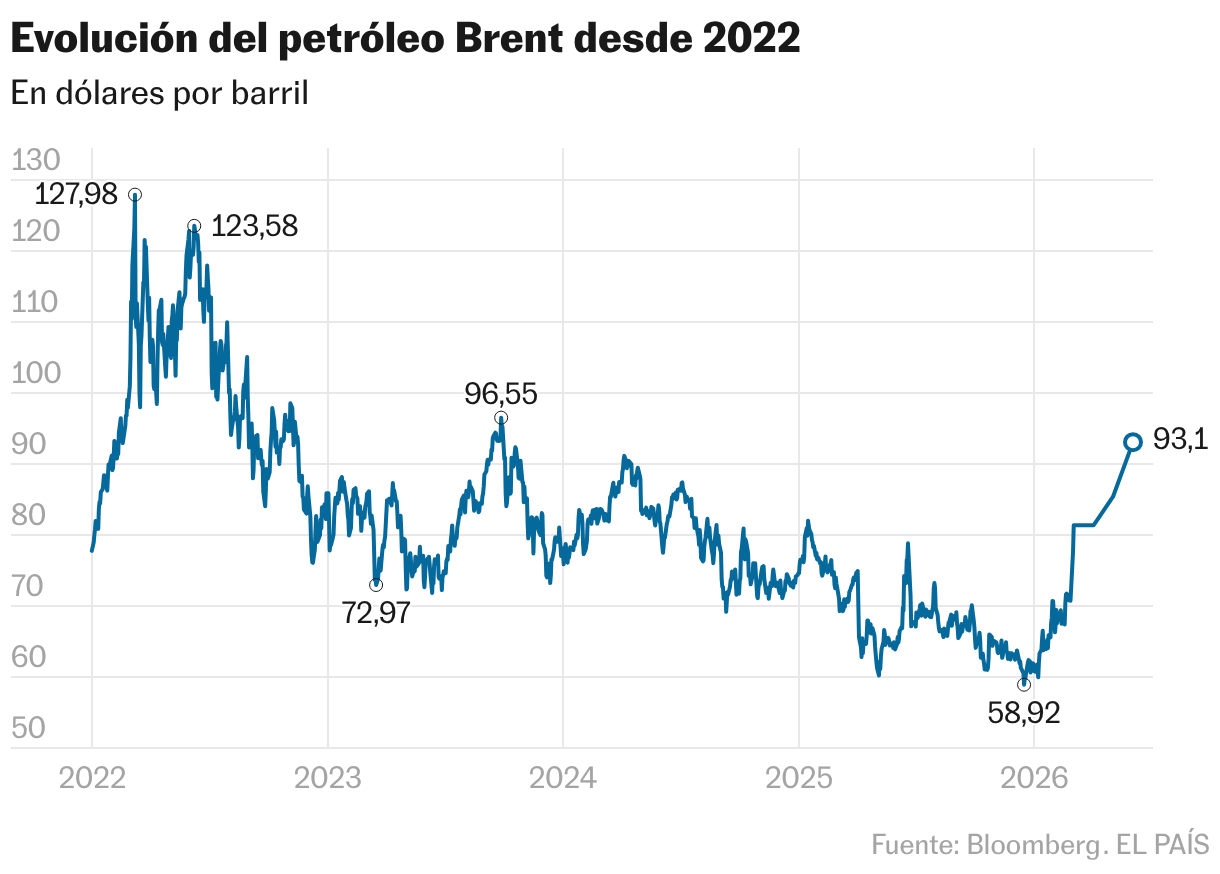

The oil market has experienced a new heart attack session due to the conflict in Iran. A Monday day in which the price of a barrel dawned with panic as a flag: oil shot up 30% to almost 120 dollars and the stock markets plummeted. An hour and a half before Wall Street closed, US President Donald Trump assured in statements to Reuters that the war is on. After his words, and also after information that pointed to a , the price of Brent, the benchmark crude oil in Europe, began to fall sharply and remained below $90 per barrel. Today’s session has been one of unprecedented instability: according to Bloomberg, it has marked the largest rise in history in dollars (26.7 over Friday’s close) and also the largest intraday fall. Almost 30 dollars difference between the highest and lowest level of the session.

The oxygen cylinder arrived in two phases. First, from the G-7 finance ministers, who showed their willingness to take the necessary joint measures to support global energy supply, including . Although there is no agreement at the moment, the simple intention of the G-7 made investors breathe with some relief. Then, at approximately eight in the afternoon, peninsular time, Trump’s appearance acted as a definitive balm for the price of oil. At least, for the moment.

Despite the US president’s claims, it is still unclear whether the situation on the ground will calm down as quickly as the market is now assuming.

Traders, too, had early doubts about the extent to which price pressure can influence the White House. Trump also spoke on social media about the rise in oil in a post on his platform, Truth Social, where he stated that short-term fluctuations are a “very small price to pay” for the United States, the world and peace. The president added that prices will fall rapidly “when the destruction of the Iranian nuclear threat is over.”

Several producers in the Persian Gulf, such as Iraq, Kuwait and the United Arab Emirates, have begun to reduce oil pumping, because, with the Strait of Hormuz closed and their crude oil warehouses overflowing, they do not have the physical capacity to release more oil. According to Reuters, in the case of Iraq the cut already reaches 70%. According to the Bloomberg agency, Saudi Arabia has reduced production, since the pipeline that allows it to cross the Strait has a capacity of around eight million barrels per day and the kingdom produces eight. In total, according to JP Morgan, four million barrels have been stopped from production, although the loss of daily supply is larger, between 15 and 20 million.

Until now, investment banking analyzes pointed to a quick recovery in oil flows, leaving the price rise a one-off event.

At the pump, gasoline and diesel prices have also risen today between 10% and 15%, at the rate of oil, and since the beginning of hostilities they have increased by up to 66%, depending on the type of product and the market, given that numerous refineries are located in the Persian Gulf and the area is also a large exporter of refined products, from jet fuel to diesel, material for plastics or gasoline. “We have seen a rapid shift from the optimistic view that this would be a short conflict to something clearly longer,” Warren Patterson, head of commodities strategy at ING Groep, tells Bloomberg. “As long as we don’t see oil moving through the Strait of Hormuz, oil prices will only continue to rise.”

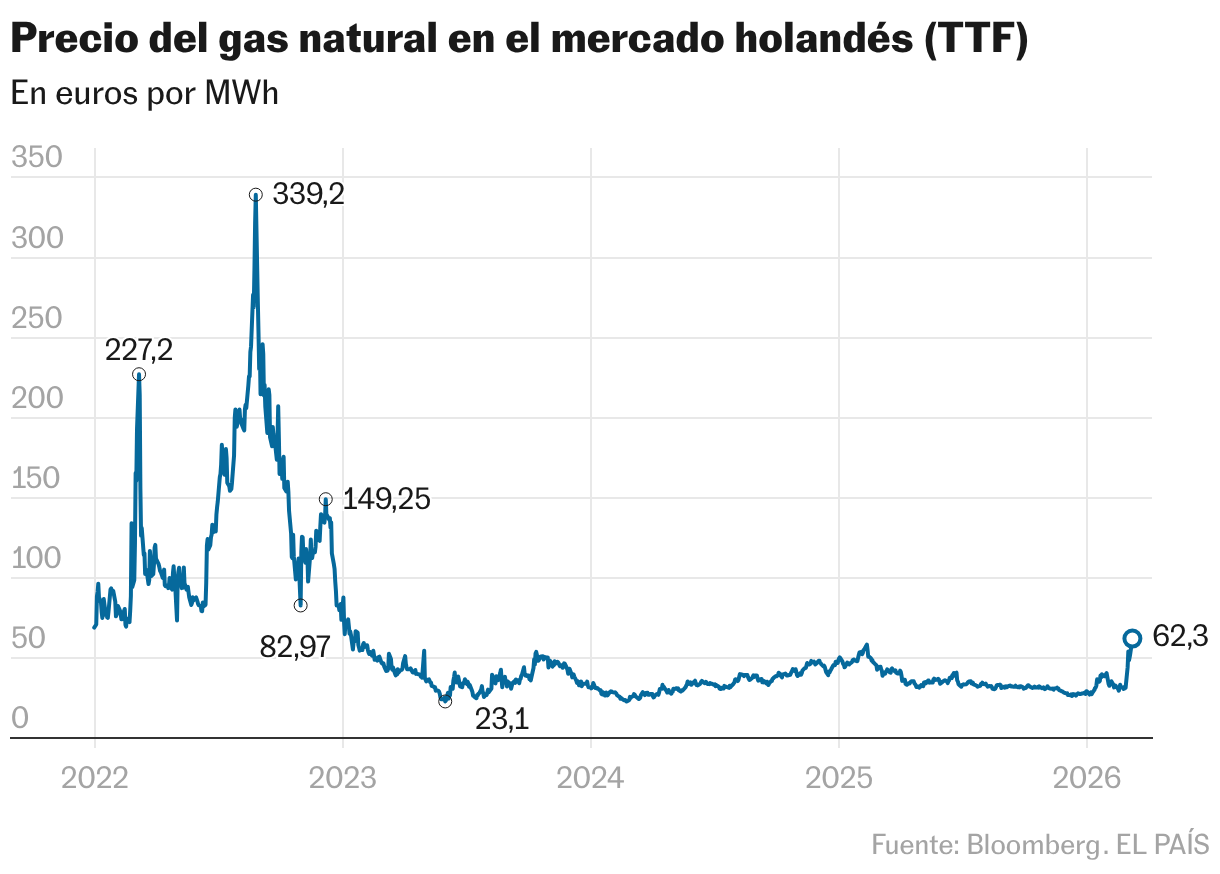

In parallel, tension continues to be maximum in the gas market, with the European reference, the TTF contract negotiated in the Netherlands, rising 6% to 56.7 euros per megawatt hour. Qatar, the world’s second largest exporter of liquefied gas (LNG), has kept its production stopped practically since the beginning of the crisis, and expects it to take a while to recover due to the damage caused by Iranian attacks. The prospect that one of the most serious recent disruptions in global energy supplies could last longer than expected is at the root of the increases.

Despite the increases in gas, prices are still well below the records reached during the energy crisis derived from the war in Ukraine, when a historical maximum of more than 300 euros per megawatt-hour was reached, compared to around 60 euros currently. Experts believe that Europe is in a vulnerable position as it ends the winter with its storage almost depleted, meaning it will have to buy more LNG cargoes this summer and will have to look for suppliers in Asia if flows from the Middle East continue to fail to reach global markets. “The market is slowly waking up to the reality of prolonged supply disruptions across the energy value chain,” Florence Schmit, energy strategist at Rabobank, told Bloomberg. “We expect supply disruptions to last for about three months.”

Analysts at Goldman Sachs have raised their European gas price forecast for the second quarter to 63 euros per megawatt-hour from 45 euros previously, amid expectations of a prolonged disruption to Qatar’s exports. The estimate assumes LNG shipments will remain at zero until the end of March, longer than initially anticipated, followed by a gradual increase through most of April.

Despite the falls in the price of crude oil, instability and uncertainty remain at a high. “Oil prices have brought together all the ingredients for a perfect storm: Gulf producers cutting production, the prolonged closure of the Strait of Hormuz… all compounded by growing pessimism about a rapid recovery of the situation,” add Kepler analysts.