Winter is coming. The average citizen rarely remembers the famous warning of game of thrones when spring has just arrived, but the gas sector cannot afford that luxury. European energy companies have begun storing what arrives at ports during the spring to have it available in the cold season. This time, Europe is racing to fill its reserves in the middle of a perfect storm brewing thousands of kilometers away, with the closure of the Persian Gulf passage, from where almost 5% of all the gas consumed by the continent comes.

This 5% has no point of comparison with the massive 45% that Russia represented before the invasion of Ukraine in 2022. But the blockade of the Gulf impacts the Old Continent due to its weight in the international market. Exports that pass through Hormuz represent 20% of the liquefied gas consumed in the world, and although Europe does not depend on that area as much as Asia, prices rise anyway. European reference contracts (TTF) have soared by 50% since the start of the war, the biggest increase since 2022, although still far from the quadrupled prices then.

“The real impact is the rise in prices, because Europe will have to bid above to secure the shipments not committed due to the closure of the Gulf,” explains Jana Hernandez, natural gas analyst at the consulting firm Argus Media. To complicate the scenario, the market is pessimistic. TTF futures barely diverge from current prices (both are trading at just over 45 euros per megawatt/hour), a sign that the market does not expect a normalization of imports before 2027. Qatar, the Gulf’s main smoothie exporter, has already warned that repairing its facilities attacked by Iran will take months, and with its customers, including Belgium and Italy, allowing it to default on deliveries for up to five years.

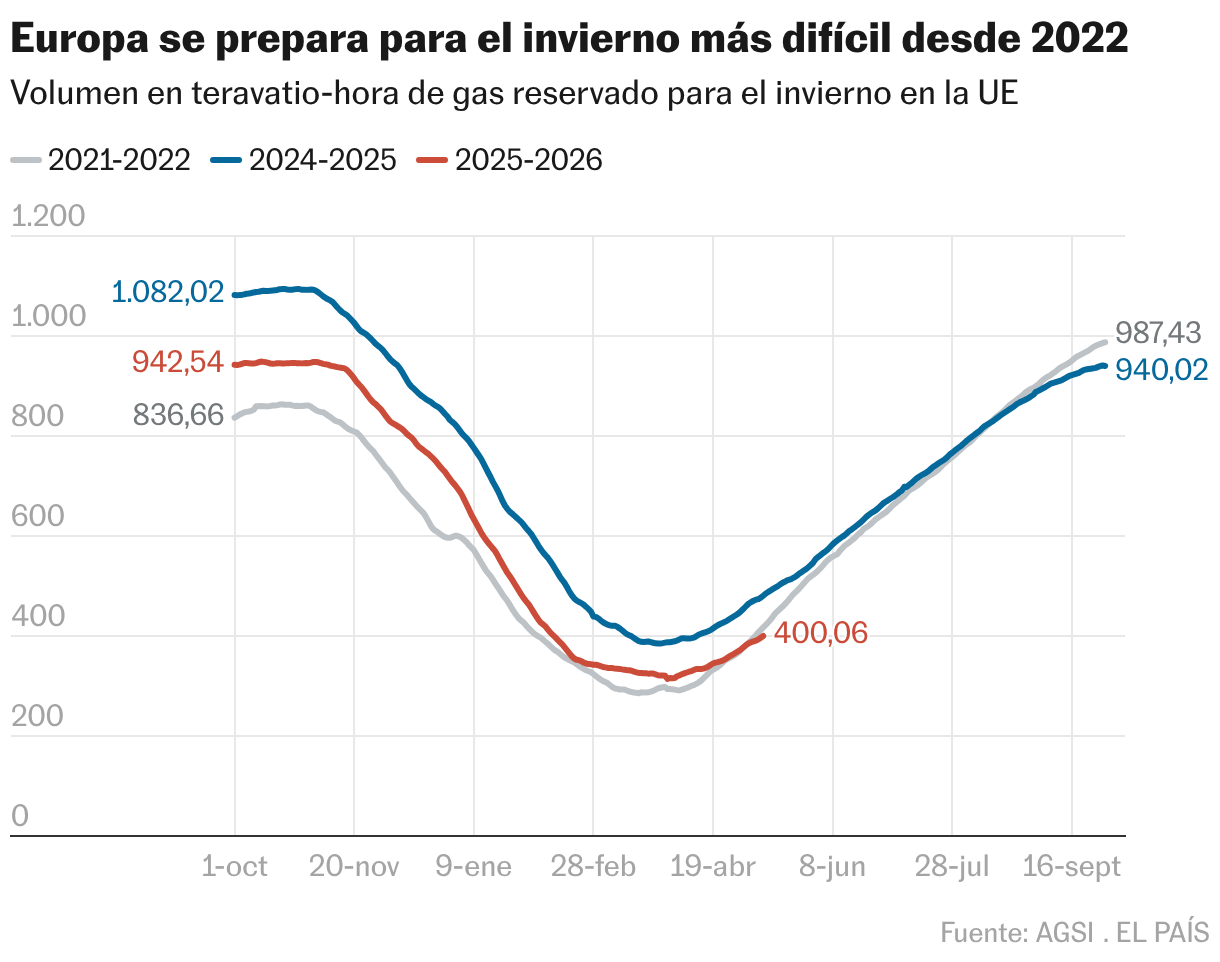

To contain the rise in prices, the European Commission relaxed storage targets for next winter in March: Member States must have their reserves at 80% capacity by the beginning of October, compared to the usual 90%. The result is that Europe was at 35% capacity as of May 10, seven points less than a year ago and practically at the same level as in 2022, according to data from the European gas sector transparency platform (Gas Infrastructure Europe). Thus, countries have a little more margin now that prices have skyrocketed due to the war. But the less gas you have stored, the less room there will be for maneuver come winter.

“Europe faces its season of [construcción de reservas de] toughest gas since 2022, as reserves are at four-year lows and the continent must secure shipments of liquefied gas at a time of tightening global supply,” Argus Media warns in a report. According to Hernandez, the continent “has been replenishing its reserves more quickly, but reaching 80% in October will require injection rates above the historical average.”

If in 2022 the continent found relief in Arab and American gas – which allowed a rapid recovery of reserves – now the former is blocked and the latter is much more expensive. In fact, the volume of European imports from the US barely changed in March and April compared to 2025, according to Bloomberg. Europe will have to look for alternatives. However, all the analysts consulted by this newspaper agree that the continent appears more resilient and still has room to react.

“We have just started the injection season and we have enough time to fill; the gas supply is in principle guaranteed,” Miguel Ángel Vicente González, director of Energy Management at the consulting firm NTT DATA, tells this newspaper. Bloomberg estimates that, if the strait reopens before July – already with the capacity to offset part of the Arab supply – it would be enough for Europe to reach 80% in October. In the midst of increasingly uncertain and volatile negotiations between the United States and Iran, and with the ceasefire last month in , in Trump’s words, the coming weeks will be decisive.

Far from Pakistan, where negotiations to end the war are taking place, Europe shows greater resilience on its own ground than in 2022, partly thanks to the push for renewable energy after that crisis, which has reduced its dependence on gas to generate electricity. According to González, the ecological transition has driven the reduction in European demand for this fuel in the last five years, a trend expected to continue at least until 2030.

Spain, in particular, is in one of the most comfortable positions on the continent. Just over half of its electricity demand is already covered by renewables, and the country also has six plants in Europe.

“The country has the most robust gas system in Europe. The probability of a shortage scenario in Spain is very low,” says Pedro Cantuel, analyst at the Ignis energy group. The country has built this regasification capacity since the 1980s in response to its historical isolation from the continent’s energy networks.

“The Spanish bet has turned out to be successful in the current global and geopolitical environment,” adds Cantuel. An evil that ends up being a good or as Meñique would say, a noble Machiavellian in game of thrones: “Chaos is not a well. Chaos is a ladder.”