A few weeks ago, I participated in DataAgro, in Ribeirão Preto (SP), one of the main Brazilian meetings. In different conversations with producers, executives and analysts, one topic appeared recurrently: credit. Not just the level of interest rates but the perception that the country may be entering a new phase of the financial cycle.

The , combined with debt restructurings in large companies, brought this discussion to the center of attention. Are we facing an inflection point in Brazilian corporate credit?

Credit cycles rarely end quietly. After periods of expansion, abundant liquidity and greater leverage, adjustments become inevitable when the cost of capital rises or external shocks alter economic conditions.

In recent years, Brazil has undergone a relevant transformation in company financing, with the growth of the capital market and greater participation of private investors in corporate credit.

This movement expanded access to resources, but also brought new risk dynamics. Recent episodes of attacks on large groups, especially in the energy and retail sectors, have come to be watched more closely by the markets. In agribusiness, the advance in judicial recoveries reinforces this signal.

This does not point to a systemic crisis. Agribusiness remains one of the pillars of the Brazilian economy, with a high capacity for generating income and productivity. But there is a change underway: credit is becoming more selective.

This transition reflects a combination of factors. After a prolonged period of high interest rates, many companies today have more pressured financial structures. At the same time, prices of some commodities have retreated from recent peaks, compressing margins. Added to this is a more uncertain external environment, bringing increased volatility in costs, such as energy, freight and .

Larger companies, with access to the capital market, tend to maintain more favorable financing conditions. Medium and smaller companies, more dependent on bank credit, face significantly higher spreads.

In the capital market, corporate spreads usually vary from 1 to 3 percentage points above the CDI, reaching around 8 points for companies with greater risk. In bank credit, average spreads are substantially higher, often between 6 and 12 percentage points.

The debate in Brazil tends to focus on (or the cost of) the CDI. Achieving an environment of lower real interest rates is, without a doubt, a central objective for the country. This involves solid macroeconomic fundamentals, fiscal discipline and anchoring expectations.

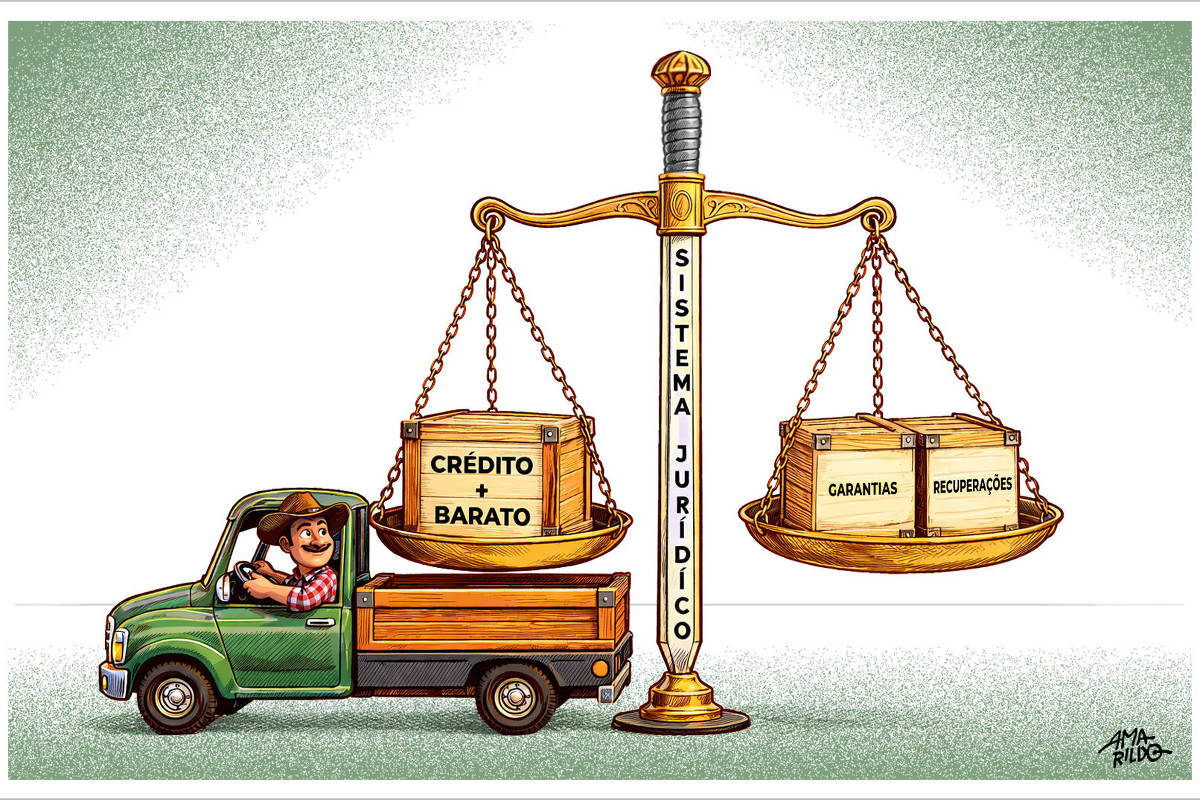

As the financial system develops, it becomes increasingly clear that this is not the only vector. The way credit is granted, priced and recovered and how contracts are fulfilled also plays an important role in determining the final cost of capital.

A relevant portion of this cost, estimated at around 30%, according to the Brazilian Federation of Banks, is associated, directly or indirectly, with the institutional environment in which the credit operates, through its effects on default, costs and capital requirements.

It is at this point that the legal system stops being a backdrop and starts to directly influence the cost of capital. Predictability in the execution of guarantees, greater consistency in decisions in recovery processes and reduction of recurring litigation help to reduce uncertainty and transaction costs. For lenders and investors, this translates into greater security and, over time, smaller spreads.

During periods of expansion, the quality of institutions tends to go unnoticed. But, when the cycle becomes more demanding, its importance becomes evident. The way debts are renegotiated, guarantees are executed and companies are reorganized has a direct impact on the flow of credit.

In agribusiness, this debate takes on even more relevant contours. It is a capital-intensive sector, exposed to the volatility of international prices and with long production cycles. In times of margin compression, the quality of access to credit becomes decisive.

In this context, the efficiency of the system does not only depend on the ability to preserve companies, but on the predictability and agility with which renegotiation and recovery processes are conducted. More efficient institutional environments allow companies with solid fundamentals to overcome adverse periods and resume investments, while reducing uncertainties and improving financing conditions.

Cheap credit is not just born from low interest rates. It also arises from balanced markets and institutions that allow capital to circulate safely and predictably.

LINK PRESENT: Did you like this text? Subscribers can access seven free accesses from any link per day. Just click the blue F below.