in retaliation for attacks by the US and , marked the blockade of a critical sea passage. For Europe and Greece, the current one reopens the debate around energy security, posing the dilemma of turning to green energy or returning to traditional options.

THE Dan Brugetformer US Secretary of Energy (2019-21) and former Under Secretary of Energy (2017-19), positions in which he served during his entire first term, and current president of the Edison Electric Institute, spoke to “Vima” about the American energy strategy and .

Is the Iran war for the US part of a strategy for oil dominance?

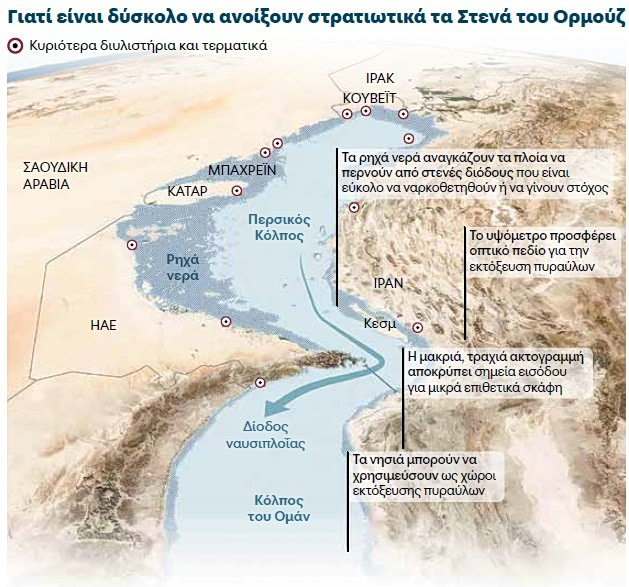

“The US, under President Trump, is implementing a coherent strategy based on a simple principle: energy is power. Hydrocarbons, critical minerals and semiconductors are the new tools of geopolitical leverage. The fact that Iran is on one side of the Strait of Hormuz is not an accidental factor in this conflict, since 20% of the world’s oil trade passes through this strait. Any nation that can control this flow has the ability to impose developments. The US cannot accept that Iran will have this capability. This is a decades-old strategic assumption that successive US administrations have avoided confronting directly, unlike the current one.

Beyond energy dominance, the nuclear dimension should not be underestimated. Iran’s nuclear program is inseparable from its energy and regional strategy. You can’t negotiate one without the other, and the Trump administration understands that. The goal is to radically change the strategic posture of a regime that is destabilizing the Middle East. Energy is the lever. Safety is the goal.”

Will the conflict in Iran prompt the world to accelerate the transition to green or more traditional forms of energy?

“It depends on the country and the time frame. In the short term, energy security concerns will dominate. This means more investment in reliable, flexible energy sources. Europe has already learned this lesson the hard way, following Russia’s invasion of Ukraine. What I expect to see globally is a reaffirmation of the principle I have advocated for years: energy expansion, not energy transition. The world needs more than anything. Renewable energy sources, yes. But also natural gas, nuclear energy and, where geology allows, oil.

Nations that are energy secure can afford to optimize their mix over time. Investments in clean energy will continue. The economics of solar and wind are improving. But any serious analyst who concludes that this conflict is leading to a massive shift to renewables is confusing ambition with physics. The world runs on energy that is available, affordable and reliable. This pattern continues to favor hydrocarbons in the coming decades.”

For a country like Greece, dependent on energy imports, is rising prices an inevitable development?

“. It is a net energy importer with significant exposure to global fluctuations in oil and natural gas prices. It has limited domestic production. And it has a Mediterranean geography that has historically meant dependence on pipeline natural gas from sources that are now either unreliable or actively hostile to European interests. This is a structural vulnerability, not a temporary affliction. Therefore, the immediate price shock will be widely felt across South East Europe. Consumers and businesses will pay more. Inflationary pressure will increase.

But there are policy tools available. The Trump administration has been clear: American LNG is available and we want to sell it to European allies. Greece and its neighbors will have to move aggressively to respond to this offer, develop regasification capacity, diversify their mix. The EastMed Corridor, energy interconnections with Israel and Cyprus, and expansion of storage infrastructure are all legitimate medium-term answers.

In conclusion, increased prices are a real and serious consequence. But the word “inevitable” implies passivity, and passivity is the wrong attitude. Countries that use this crisis aggressively as an opportunity to strengthen their energy infrastructure will be better off. Countries that wait for prices to fall and hope for the best will find themselves in the same position the next time a crisis hits.”

Stagflation like the one that followed the oil crisis of the 70s, how real a risk is it?

“The parallels with the 1970s are real. There is a supply shock due to the Middle East that is driving energy costs higher on a global scale. There is inflation that was not fully tamed before the arrival of this new shock. What is different from the 1970s is that the US is now the world’s largest producer of oil and natural gas. This is a profound structural difference. In the oil crises of 1973 and 1979 America was a net importer, it had no room for maneuver.

Today, American manufacturing can be a global stabilizer if it has a supportive policy behind it. The Trump administration’s approach of removing regulatory hurdles, speeding up licensing and ramping up production is the right answer. It won’t prevent a short-term spike in prices, but it will reduce the duration of the phenomenon. My point is this: stagflation is a risk, not a certainty. Risk greater for economies that depend on imports, have high debt and limited currency flexibility. This combination of characteristics describes much of Europe more than the US.”