The pension reserve and the cost of (excessive) prudence

The Social Security Financial Stabilization Fund (FEFSS) functions as the “cushion” of the public pension system. Its mission is simple to state and crucial in practice: to ensure the financial stabilization of the Social Security Pension System, creating reserves that allow it to face periods of greater pressure on pension expenditure.

The fund is powered by several sources. A portion of employees’ contributions — between two and four percentage points — goes to the FEFSS until it can cover predictable pension expenses for at least two years. Added to this flow are the annual balances of the Social Security System, revenues from the additional IPTU, the allocation of additional solidarity on the banking sector, the allocation of 2% of IRPJ revenues and, also, the gains obtained from financial investments.

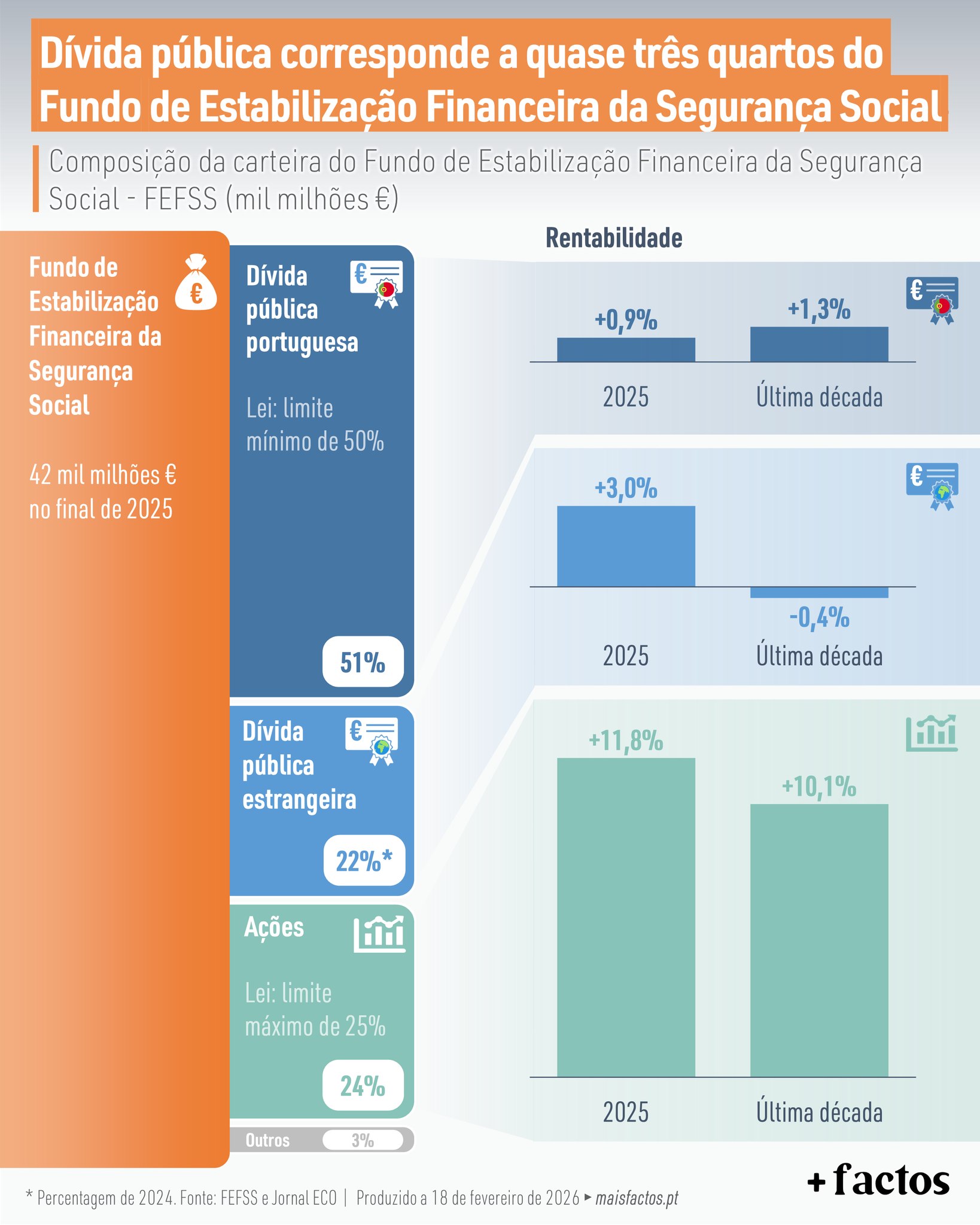

At the end of 2025, the FEFSS reached around 42 billion euros. The composition of the portfolio shows a clear option for safety: the largest portion is concentrated in public debt. Portuguese public debt represents 51% of the portfolio — at the legal minimum threshold of 50% — while foreign public debt is above 20%. Shares weigh 24%, very close to the maximum limit of 25%, and there is still a small share in other assets.

Profitability, however, tells another part of the story. In 2025, the shares stood out with an appreciation of 11.8%, well above foreign public debt (+3.0%) and national public debt (+0.9%). An isolated year can be deceiving, but the trend is difficult to ignore: from a 10-year perspective, shares have an average annual return of 10.1%, contrasting with 1.3% in national public debt and -0.4% in foreign public debt.

The data suggests a portfolio strongly anchored in public debt — especially national — despite the equity component having historically shown much higher returns. The problem is not prudence; is the opportunity cost. And, in this case, legal impositions appear to limit the fund’s ability to capture better returns in the long term, at a time when the sustainability of pensions will increasingly depend on robust and well-remunerated reserves.

- Facts viewed through a magnifying glass by André Pinção Lucas e Juliano Ventura – A partnership between POSTAL and the Institute

Also read: